![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

A Sure Sign of a Housing Bubble

Sunday, August 07, 2005

In what is further confirmation of a housing bubble, non-homo sapiens are now getting in on this sure-fire way to easy riches.

Did anyone ever think it would come to this?

Click to enlarge

In what is further confirmation of a housing bubble, non-homo sapiens are now getting in on this sure-fire way to easy riches.

Did anyone ever think it would come to this?

Click to enlarge

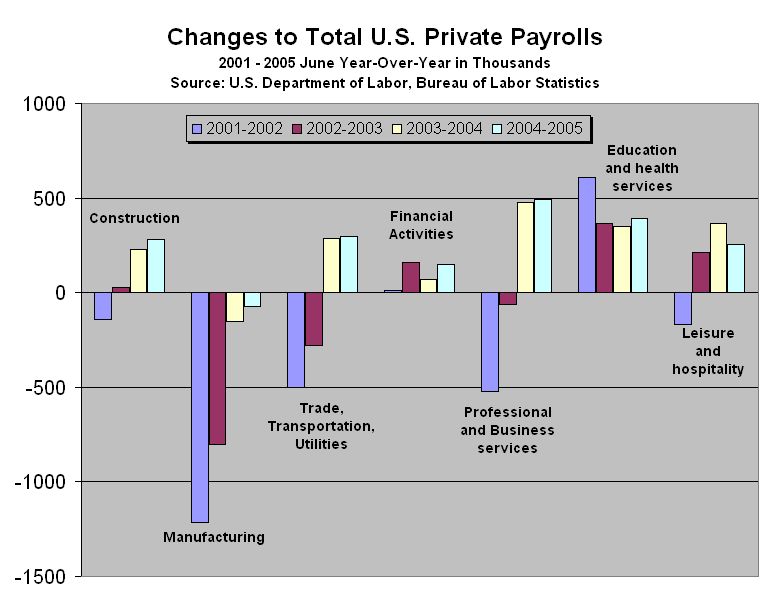

The nonfarm payrolls number came in at +207,000 today, with big gains in retail trade and food service, while the manufacturing sector again declined. The headline number was hailed as good news for the economy as it beat expectations that were around +180,000.

This report is consistent with patterns that have developed over the last few years - strength in certain areas of some sectors, most with some connection to real estate and/or the wealth effect associated with rising home values.

Today we look back at the last four years of job creation and find that outside of the education and health services sector and a few big numbers within the trade, transportation, and utilities sector, the job creation story for the last few years can pretty much be summarized as:

Now, these three groups do not cover all job creation for this period, but they cover more than you would think they should for a "normal" economic recovery - this economic recovery seems to be anything but "normal".

It appears that we have a real problem with job creation in this recovery - not in the number of jobs being created, although the totals are historically weak, but in the quality of the jobs being created. Of course, no one seems to be paying too much attention to this problem because most people are too mesmerized by the rapidly rising value of their home, and the daily quandary of what to do with all that home equity that is piling up.

So, let's look at job creation in the U.S. over the last four years. All charts are year-over-year changes from June to June starting in 2001 and ending with the June 2005 data released last month. The June 2001 date marked the bottom of the last recession.

The first chart includes all major sectors, and includes the familiar depiction of manufacturing job loss. On the surface, this appears to be a fairly broad based pattern of job creation, at least for the last two years, as indicated by the yellow and blue bars.

Click to enlarge

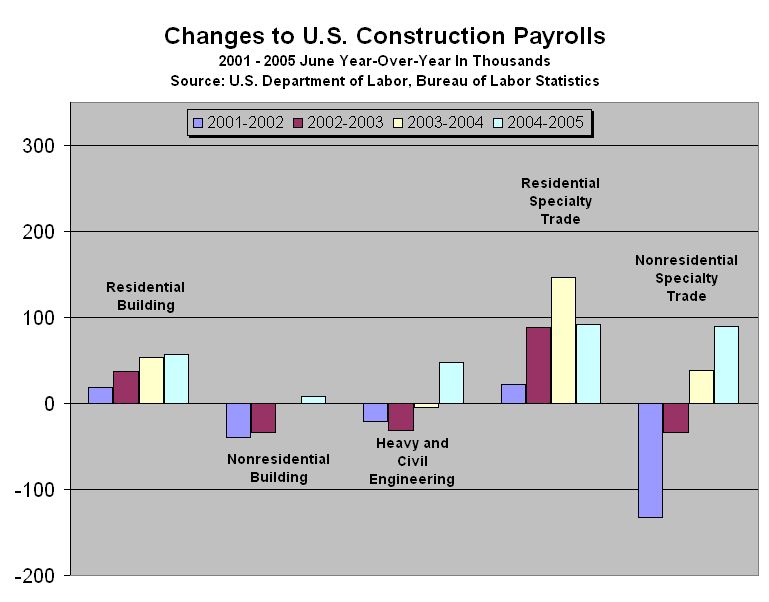

But a closer look at the sectors reveals that this high level view of job creation is not what it seems. The following charts provide details for the construction, financial activities, professional services, and leisure and hospitality sectors. The scale is the same for all four so you get a clearer picture of the relative number of jobs being created or lost by sector and by category.

[The trade, transportation and utilities sector is not included here. It includes such interesting job categories as building material and garden supply as well as trucking - both related to the wealth effect. We'll dig into these numbers some other time.]

Starting with the construction sector, we find that job creation is dominated by home construction and residential specialty trade - the specialty trade guys are the ones that have been installing granite countertops all across the country for the last few years. Only in the last year has nonresidential work picked up and it is still comparatively small.

Click to enlarge

Compared to the other sectors, very few jobs have been created in the financial activities sector - what jobs have been created, not surprisingly, are credit and real estate related. Does anyone else find it odd that only a little more than 100,000 real estate jobs have been created over the last four years? It feels like it should be a million or more.

Click to enlarge

The professional services chart is pretty disappointing - in the last year or so, it's mostly temporary jobs and employment agency jobs! It's nice to see a pick up in computer related jobs and it looks like the janitorial and lawn-mowing industries are booming, but it would be much better to have some bigger yellow and blue bars on the left side of the chart, instead of just the big ones on the right.

Click to enlarge

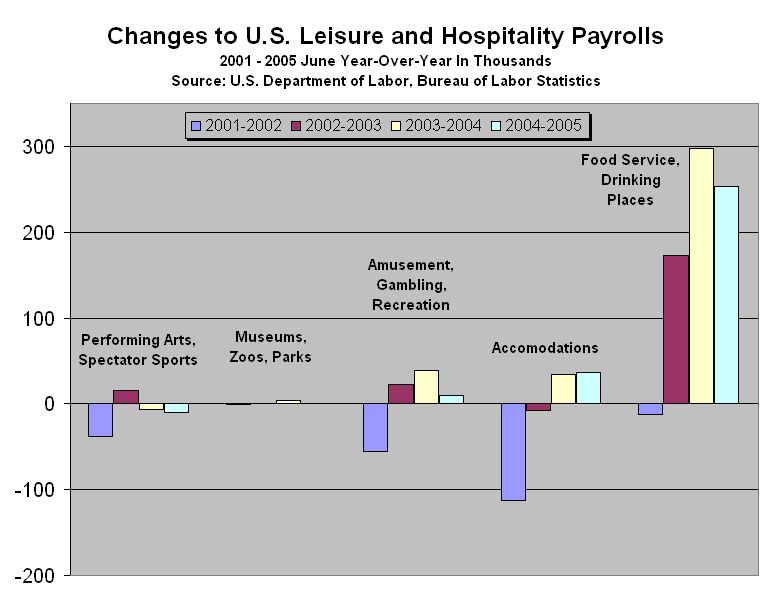

And, finally we come to the chart that tells the most interesting part of the jobs story. In the last four years, we have created about 700,000 jobs for waiters, busboys, cooks, greeters, valets, bartenders and bouncers. It looks like a lot of people are spending a lot of money eating and drinking out. Since this part of discretionary spending is the easiest and fastest to cut back on, if and when people begin feeling less wealthy due to a cooling real estate market, look for trouble in this area.

Click to enlarge

By the looks of all these charts, recent job creation really doesn't look that healthy - most people have given up on increases in manufacturing jobs, but now it seems that even good service jobs are hard to come by. Nothing against waiters, temporary help, and granite countertop installers, but these are not the type of jobs you expect from the world's economic superpower.

It seems that as long as home prices continue to rise, and people continue to feel wealthy, they will continue to spend money at restaurants and at The Home Depot, while employers remain skittish about hiring permanent help.

Wonderful!

The phrase Ponzi scheme is tossed around quite a bit these days when people talk about the housing bubble. While not truly a Ponzi scheme, the housing bubble has enough similarities with this notorious scam that it is worth taking a look at.

Named after Charles Ponzi, an Italian immigrant at the turn of the last century who became one of America's best known swindlers, this scheme was used effectively by its creator during six months in 1920 to amass millions of dollars in personal wealth. While millions of dollars doesn't sound like much today (perhaps a few mobile homes in Malibu), in 1920, this was a lot of money.

The scheme was eventually found out by Clarence Barron, the founder of Barron's financial paper, when a few simple calculations proved that the business for which Mr. Ponzi was gathering investment money was theoretically impossible. That, plus the fact that Mr. Ponzi invested none of his own money in his venture.

A Ponzi scheme is defined by Wikipedia as:A fraudulent investment operation that involves paying returns to investors out of the money raised from subsequent investors, rather than from profits generated by any real business. A Ponzi scheme offers high short-term returns in order to entice new investors. The high returns that Ponzi schemes advertise require an ever-increasing flow of money from investors. Once the flow of new investment stops, the scheme is doomed to collapse.

As this relates to today's housing bubble, the part about high short-term returns enticing new investors is certainly true, as is the requirement for an ever-increasing flow of money. We have the world's central banks and still burgeoning finance industry to thank for the ever-increasing supply of money - it is individual home purchasers who make the money flow.

It seems the only characteristic of a Ponzi scheme that doesn't match up neatly with the housing bubble is the part about paying returns to previous investors out of the money raised from new investors, rather than from profits generated by a real business.

When you think about it though, this isn't too far off the mark. Today, existing homeowners are seeing rapid appreciation as a result of money coming into the real estate market from new homeowners, rather than from "naturally" rising home values (i.e., home values driven by such factors as population, wages, rents, etc.).

So, instead of there being no real business to generate profits in a true Ponzi scheme, it is a question of how "unnatural" the rapid rise in home prices is today. This is not nearly as cut-and-dried as the discovery that Clarence Barron made 85 years ago, but as the days go by and more respected analysts and economists weigh in, it increasingly appears that today's real estate market is not very natural at all - some would say today's real estate market is not theoretically possible.

The last sentence in the definition above will surely determine whether the current housing bubble will be thought of as a Ponzi scheme five or ten years hence:Once the flow of new investment stops, the scheme is doomed to collapse.

At some point, the flow of new investment in real estate will slow down dramatically. Obviously it won't stop completely, because people will always be buying homes - they'll just stop buying them two or three at a time.

If, when this happens, home prices moderate or decline slowly waiting for wages and rents to catch up, then it won't really be fair to call today's housing bubble a Ponzi scheme.

If, on the other hand, home prices do collapse, today's housing bubble will most likely be called The Biggest Ponzi Scheme Ever.

Back in late 1999, when Senator John McCain was running against then-Governor George W. Bush in the Republican primaries, he was asked whether he would reappoint Alan Greenspan as Federal Reserve Chairman if he was elected president. McCain replied, “Not only would I reappoint him, but if he died we’d prop him up and put sunglasses on him like they did in the movie Weekend at Bernie’s.”

Everyone had a good laugh.

With Mr. Greenspan's scheduled retirement next January drawing ever near, few people are laughing today, and for good reason.

The Issues

As discussed in this article from the Financial Times, there is great concern about the transition from the current Fed chairman to the next. The major issues the incoming chairman will have to deal with are:

Honest!

Here are the issues, in excerpt form, from the article. You read 'em and see if the above summary isn't accurate:1. "Although the US is outperforming most other industrial economies, it is borrowing heavily to sustain a massive wave of spending. This poses no immediate problem for the US, but when the economies of Europe and Japan return to robust levels of expansion, the Fed will have to decide how to respond to the likely increases in domestic inflation and a falling US dollar."

The Dream Team that Isn't

2. "Even before that happens, the new chairman must formulate a monetary strategy for an ageing economic expansion that, on the day he or she takes office, will be in its fifth year. While it is unlikely that the current expansion will end next year, the challenges of guiding the economy on a sustainable path can only grow in coming years, especially if oil prices continue to rise."

3. "The new chairman will need to make tough judgments on the housing sector. Unfortunately, the Fed does not yet view this with alarm. It has drawn attention to isolated instances of exuberance while publicly applauding aggregate data on housing activity and the financial strength of households. Nevertheless, household debt has risen sharply, and the grave risks this poses can be minimised only by low interest rates, rising household income or a combination of the two. For the new chairman the question will be: can households continue to serve as a stabilising force in the next recession or have they already been marginalised by the household debt binge?"

4. "This approach [measured rate hikes and transparency] has wrought several unintended consequences. For one, it has contributed to a massive carry trade - borrowing in low-yield funds to invest in higher-yielding ones. This is because investors have been conditioned to expect moderate and steady increases in money rates, which their quantitative analysis shows will pose limited risks, if any, along the yield curve. This, in turn, has led them to conclude that the carry trade can be the source of substantial profits. As a result, the yield curve spread has compressed significantly. Although spread compression typically yields smaller profits from carry trades, profits have remained high as investors have enlarged their positions."

5. "The second unintended consequence of the Fed's measured response policy has been the massive growth of debt. Investors have reacted to the assurance of a measured response by borrowing more. In highly securitised and innovative financial markets, which by themselves encourage entrepreneurial financial behaviour, rapid debt growth is a natural consequence of measured response policies. When uncertainty is reduced, risk-taking increases. Non-financial debt has increased at an annual rate of about 9 per cent during the past one-and-a-half years, while nominal gross domestic product rose 6 per cent over the same period. In the short run, this has buttressed economic expansion. But continuing to follow this approach will bring trouble down the road for the economy and for financial markets."

Lest anyone think that there may be some reason for concern when the current Fed chairman retires - that perhaps some little pin-prick somewhere will cause a snowballing loss of confidence in the absence of Mr. Greenspan - we refer back to one of our favorite articles from The Economist. This blunt assessment of how the Bush economic team might respond to a financial crisis may perhaps elevate what was a moderate level of concern into more of a panic:"In theory, Mr Bush's economic team is headed by John Snow. The president was on the point of sacking his treasury secretary at the end of last year; he then pulled back—but only apparently to keep Mr Snow as a travelling salesman for his pension-reform scheme. The former railroad boss has recently visited such well-known global financial centres as San Antonio, Albuquerque and New Orleans.

Maybe we should heed the advice of John McCain - extend Mr. Greenspans term until he dies, then prop him up like they did to Bernie in the movie.

...

Mr Bush clearly prefers businessmen and true believers to academics and Wall Street types.

...

There are two growing suspicions about Mr Bush's approach to economic policy. The first is that he sees it mainly as a question of salesmanship. Showing an admirable faith in markets, the president seems to think that economic policy will basically run itself; what you need is a bit of pizzazz to sell the president's reforms. Hence, the White House's enthusiasm for Carlos Gutierrez, the new commerce secretary, who made his fortune selling breakfast cereal at Kellogg.

The second suspicion is that loyalty is more important than knowledge. That was Mr O'Neill's problem: he said that more tax cuts were a bad idea. Larry Lindsey, Mr Bush's bumptious first chairman of the National Economic Council, was pushed out soon after he made the impolitic (but pretty accurate) point that the Iraq war could cost $200 billion.

...

In other words [in the event of a crisis], it would all come down to Mr Greenspan. But the Fed chairman is due to step down early next year. There are three front runners to replace him: Glenn Hubbard, who is well regarded but still seen as a fiscal rather than monetary expert; Ben Bernanke, a former economics professor from Princeton and now a Fed governor; and Martin Feldstein, a fiscal expert from Harvard and head of the Council of Economic Advisers in the Reagan era.

None of these men has recent experience of dealing with financial crises. That was true of Mr Greenspan once too; he earned his spurs by coping with the 1987 stockmarket meltdown. But given the lack of strength within the administration, the risks now are surely higher. Mr Bush should be crossing his fingers that nothing goes wrong."

As the consensus grows that the complete inflation of another asset bubble draws near - first stocks, now housing - many financial writers and elected officials are asking the question, "Why hasn't the Federal Reserve done something about all the crazy lending practices fueling the housing bubble?"

During the Humphrey-Hawkins testimony a couple weeks ago, Congressman Jim Saxton asked a number of questions (pdf) of Federal Reserve Chairman Alan Greenspan regarding banking regulation as it relates to current lending practices. As detailed in yesterday's fine post by Calculated Risk over at Angry Bear, it seems that the short answer from the Fed is, "That's not my job".

The Federal Reserve is apparently not much interested in the goings on at local real estate offices and mortgage lenders and is, to a large degree, turning a blind eye to the absolutely wacky home prices and lending terms that have developed in recent years. Their interest is in the soundness of the banking system - the monitoring of reserve requirements and mortgage delinquencies and default rates, which to date have not been problematic.

A few months ago the Federal Reserve and a number of other agencies issued guidance regarding home equity lending, but as reported in the New York Times recently, these guidelines seem to have been largely ignored.

So where does that leave us? Everyone cross their fingers and hope for the best?

Or, as Mr. Greenspan commented a few months back, "If there's a crisis, we'll all get together and solve it - or hopefully solve it."

A Few Examples

In what is probably the best example of the lack of effectiveness of the Home Equity Lending Guidelines from a few months back, a recent radio advertisement for a local Southern California lender hawking home equity loans made very clear that the only thing required to get a new home equity loan was equity in your home. You don't need a job or good credit - apparently all you need is an appraisal and your most recent mortgage statement. They'll take it from there.

But, it is not the Fed's job to do anything about this - they've issued guidance.

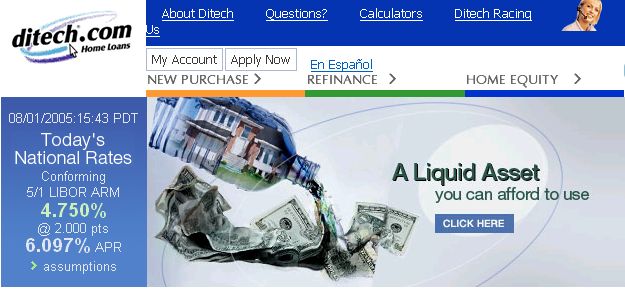

One of the better graphics to illustrate the home equity borrowing phenomenon is at Ditech.com, where they fancy rising home prices as something that can be stored in a bottle, then dispensed as necessary whenever the homeowner desires:

Click to enlarge

That's a house inside the bottle, and it is pouring out money. Nice!

Along with GMAC, Ditech.com is about the only part of General Motors that is profitable these days, and it is more than ironic to hear ads for Ditech.com home equity lines of credit intermingled with debt counseling ads on radio and television - kind of a like a choice between more booze or some freshly brewed coffee. Most people probably choose the former.

Again, not the Fed's job to discourage this sort of thing - the banks are sound.

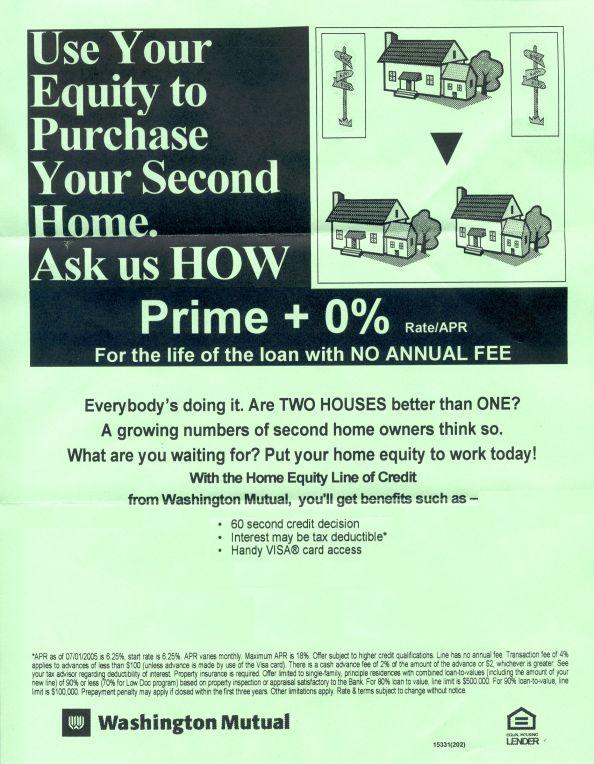

And finally, showing up in the mailbox yesterday was this gem from Washington Mutual:

Click to enlarge

Another nice graphic - this one more for its simplicity rather than the actual artwork - one house turns into two houses. And, it's OK because "Everybody's doing it. What are you waiting for?"

If not the Fed, then whose job is it to protect today's lenders and borrowers from each other?

You'd think that if no one wants to regulate lending practices, the least they could do is regulate lending advertising. That would be a good start.

Of all the items that have been published on this blog, there is one chart that keeps popping back into my head - the chart of job creation in San Diego, California over the last fifteen years, broken down into five-year segments.

It recently became clear why this chart keeps re-entering my consciousness.

It seems that the mainstream financial media and the White House are now in the midst of a massive "anti-housing bubble" media blitz - an obvious attempt to counter all the housing bubble analyses and articles that have been showing up online and in local newspapers over the last few months. Apparently, this is an attempt to avoid a calamity where everyone wises up at the same time - drive home some simple talking points so no one panics.

Based on having read so many convincing analyses and articles making the case for the existence of a housing bubble, by many highly respected analysts and scholars, each time one of these "anti-housing bubble" stories reaches my ears, my reflexive response is to think of this chart.

We'll get to the chart in just a minute.

Rose Colored Glasses

It seems that Treasury Secretary Snow, Commerce Secretary Gutierrez, Chief White House Economic Adviser Bernanke, and other White House representatives are all popping up on CNBC or writing articles for mainstream business publications, all carrying the same message:

Economists and real estate executives appear on CNBC or write more articles for business publications making the case that the housing market is driven by strong fundamentals - a healthy economy with strong job growth and low mortgage rates which are in large part due to low inflation expectations.

On the surface this all sounds so good, and surely, many people who hear these numbers repeated over and over feel assured that all is well, despite what they see happening in the labor market or with prices they pay for goods and services. Anyone who knows the details of how these statistics are calculated, knows that they don't tell the whole story, and in fact are, by design, consistently overstating real growth, understating inflation, and misleading when reporting unemployment.

The one government statistic that is not regularly questioned is the non-farm payrolls number reported on the first Friday of each month - the July report is due at the end of the week. Non-farm payrolls have increased nationally by over 3 million since the spring of 2003 when the current recovery kicked into gear. And, while this job creation is quite low by post-war recovery standards, no one really disputes that these jobs have been created.

It is the type of jobs being created that make today's economy and this economic recovery atypical - an economy far too dependent upon housing related jobs and rising real estate prices.

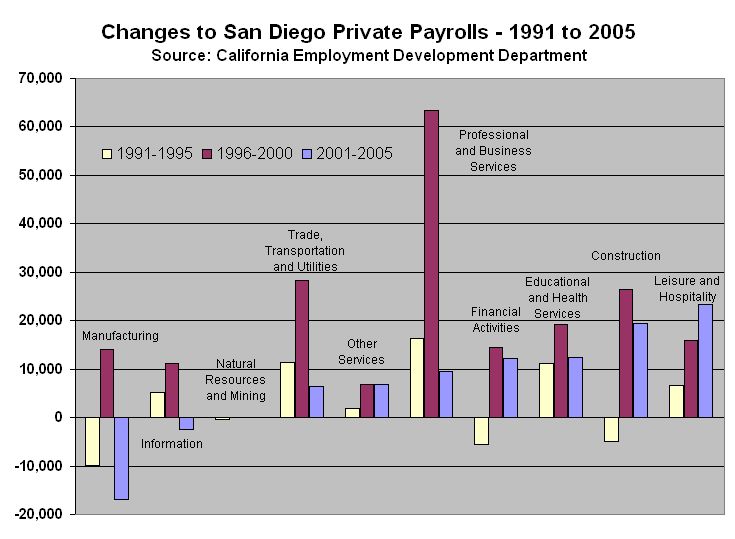

The Chart

So, here's the chart - straight from the California Economic Development Department, having previously appeared in this post a couple weeks back. While San Diego does not necessarily representative the rest of the country in its job creation trends, it does demonstrate the unhealthy relationship between the economy, job creation, and the housing bubble in this one area - this being one of the most mature housing bubbles in the country.

Click to enlarge

If you look at the three periods, what first stands out are the red bars. The red bars are much bigger than either of the other bars, as they represent the late 1990s technology jobs boom where nationally, over 14 million jobs were created in this five-year period. And, look at all the Professional and Business Services jobs - legal, architectural, engineering, scientific research and development, technical services, etc. Most people find it easier to accept the decline in manufacturing jobs when good services jobs are abundant. The relative weighting of job creation by category also seems reasonable. For 1996 to 2000, the top three were:

Looking at the yellow bars shows a dearth of new jobs, and notice the net loss of construction jobs over this period - this was during the last housing decline in Southern California, when prices fell up to 40% in many areas from their 1990 peaks. During this period from 1991 to 1995, again the relative weighting of jobs by category seems reasonable:

Finally, the blue bars - the unhealthiest of all bars. In this data set, Professional and Business Services ranks fifth! Knocked out of the top spot of the previous ten years, even trailing Financial Activities, which includes the recently hot job categories of Credit Intermediation and Real Estate. The top three this time are:

We can ignore Education and Health Services, as it is not germane to this discussion - this category has been a steady producer of jobs both nationally and locally, but has little to do with the housing bubble. Construction jobs, on the other hand are quite germane to this discussion. In fact the ratio of Construction jobs to Professional and Business Services jobs for the two periods 1996-2000 and 2001-2005 is probably the most disturbing part of this entire chart. The relationship between these two categories, roughly a two-to-one ratio, has completely switched between these two periods:

When you see what happened to the Construction category during the last housing decline in the early 1990s, it is hard not to think that there will be some severe repercussions to the economy as a whole, if there is a significant decline in demand for construction workers and specialty trade contractors (e.g., granite countertop installers).

Lastly, the Leisure and Hospitality category, leading all other categories over the last five years, consisting predominantly of restaurant help, does not seem to indicate a strong base for future economic expansion - not if people begin to cut discretionary spending in the wake of stagnating home prices and the eventual reversal of the housing wealth effect.

Pollyannas

Every time a cabinet member speaks about the health of the economy, or a Wall Street economist opines about historically high home ownership rates, or the CEO of a home building company remarks about the strong fundamentals that power today's housing market, this chart comes to mind.

It is a picture of the job market in one part of the country that clearly shows an unhealthy response to the monetary and fiscal stimulus applied after the stock market bubble burst in 2000. While this is only one county in California, the job creation patterns evidenced here are surely similar to many other areas in the U.S. - job creation that is based far too much on housing and rising real estate values, rather than what one would expect from a healthy service-based economy.

What category will lead the way in job growth for the rest of the decade?

Probably Education and Health Services.

© Blogger template Newspaper by Ourblogtemplates.com 2008

Back to TOP