![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

Debt Takes No Holiday

Tuesday, February 07, 2006

Grinding debt payments seem to be taking their toll on the good citizens of the United Kingdom. In 2005, bankruptcies shot up 45 percent from the previous year to a new record of nearly 68,000, and analysts have already predicted that the total for 2006 could exceed 100,000.

These are bubble-like growth rates.

The number of foreclosures for the year topped 10,000, an increase of 70 percent from 2004, and household debt exceeded $2 trillion. While accounting for fewer than 15 percent of the total European Union population, the British account for two-thirds of EU credit card debt.

The British are very much like we Americans.

They are one of only a handful of nations with both a trade deficit and a budget deficit, and while avoiding the disgrace of a negative number like the U.S., their savings rate has recently been in the low single digits.

Observers have often stated that the U.K. housing market is nine months to a year ahead of the U.S. housing market. If this is true, it appears that the timing of last October's new bankruptcy rules here in the States was near perfect.

The Left Coast

Out here in California, foreclosure notices are beginning to rise briskly. Nearly 15,000 default notices were sent to California homeowners in the fourth quarter of 2005, up 20 percent from the previous quarter and up 15 percent year-over-year. These rates are still very low by historical measures. A decade ago, at the bottom of the last real estate cycle, a record 60,000 notices were mailed during a single three-month period in 1996.

These rates are still very low by historical measures. A decade ago, at the bottom of the last real estate cycle, a record 60,000 notices were mailed during a single three-month period in 1996.

Throughout the 1990s, the number of notices averaged over 100,000 per year, almost double the annualized rate from the last quarter of 2005.

With home equity typically in the hundreds of thousands of dollars after the last five years of soaring housing prices, and with willing lenders eager to do business, it's a wonder how 15,000 households fell behind on their payments last quarter.

Maybe they were too busy out spending their home equity to remember to send in their mortgage payment.

There are noticeable signs of distress however. If you're interested in just how much distress is already working its way through the system, you might consider a free one-week trial offered by foreclosure.com. You can take a look at your neighborhood, or any neighborhood for that matter, and see how the homeowners in your area are faring.

It is probably way too early to think about buying distressed property, but this exercise does give a good indication of how people have managed their finances in recent years.

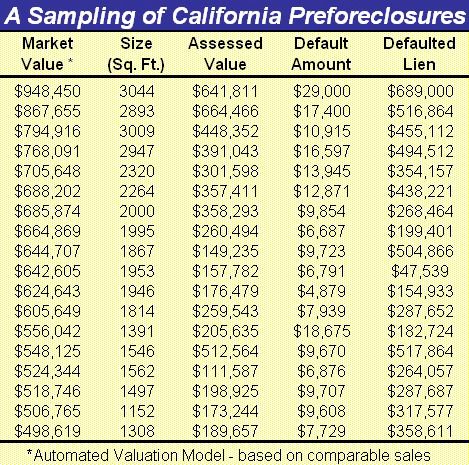

Here's a chart listing some of the preforeclosed properties in our area (this information has gone a long way in helping me explain to my sometimes skeptical wife how so many people around us appear to be so wealthy).

The term preforeclosure refers to the period of time beginning with a lender notifying a borrower that their loan payments are behind, also known as a default notice. Most people (like two of our neighbors) probably don't realize it, but when this happens, certain key information about their finances becomes public knowledge.

Oops!

Given the way that Proposition 13 works in California, much can be learned from the chart above. As in most areas, the assessed value is initially determined by the sale price of the home. Proposition 13 then restricts the rise in assessed value for homeowners who stay put.

So, for example, the last preforeclosure listed, where the market value is over two and a half times the assessed value, indicates that the owner has been there for quite a while and originally paid very little compared to the current market value of the property.

In this case, a reasonable guess would be that the home was purchased twenty years ago for a price somewhere in the low $100,000 range.

This owner has parlayed that original investment into a total outstanding debt of over three times the original loan amount, but is now having difficulty making payments.

What a country!

The outstanding debt is still well below the market value, so there is still an "equity cushion", as Alan Greenspan used to refer to it, however, the cushion appears too inflexible, in this case, to avoid falling behind on the debt repayment schedule which was previously arranged.

While the $10 per week fee charged by foreclosure.com is a bit steep, for housing bubble watchers it may be money well spent.

The Gillette Fusion five blade razor was without a doubt the stupidest commercial (it actually has a sixth blade on the opposite side of the razor where the first five are housed).

The Gillette Fusion five blade razor was without a doubt the stupidest commercial (it actually has a sixth blade on the opposite side of the razor where the first five are housed).