![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

The Bush Economy

Tuesday, November 07, 2006

Now don't fret - there will be no political views proffered here today. But, as millions of Americans head to polling stations all across the land, it's difficult not to look at things a little differently on this day.

It's hard not to think about the impact that divided government might have on both the broad economy and government spending over the next two years, as it seems all but certain that control of the House of Representatives will be changing in January.

From the most recent issue of The Economist comes this king-size story of the past, present, and future of the Republican majority beginning and this account of spending largess with origins in the last memorable mid-term election in 1994.Twelve years ago, Newt Gingrich and his Republican footsoldiers swept to control of Congress by promising to slash federal spending. For a while, they kept that promise. Between 1995 and 2000, with a Republican Congress acting as a check on a Democratic president (and vice versa), real federal spending per head remained nearly frozen. When Mr Bush took office, however, Republican lawmakers were reluctant to restrain their own man. In Mr Bush's first five years real per head federal spending grew by 3.1% annually, making him the most fritter-happy president since Lyndon Johnson (see table). Under Mr Clinton, the number of federal employees shrank by 200,000 (excluding the armed forces and postal service). Under Mr Bush, it rose by 79,000.

Remember the details of the Medicare bill back in 2003? William Niskanen, a former economic adviser to Ronald Reagan, speculates that divided government itself may be the key to fiscal restraint. Using data going back to Harry Truman's time, he found that real annual growth per head in federal spending averaged 1% under divided government and five times that under unified government.

William Niskanen, a former economic adviser to Ronald Reagan, speculates that divided government itself may be the key to fiscal restraint. Using data going back to Harry Truman's time, he found that real annual growth per head in federal spending averaged 1% under divided government and five times that under unified government.

With no hostile Congress to block him, Mr Bush has been free to follow his political instincts. There was once some ambiguity about what these were. When he first ran for president, he said he believed in limited government, and boasted that if his race with Al Gore were a spending contest, “I would come in second.” But he also distanced himself from Republicans in Congress by accusing them of “balanc[ing] their budget on the backs of the poor.”

Once in office, he appointed a budget director with a reputation for frugality, Mitch Daniels, who even tried—unsuccessfully—to make the phones at the Office of Management and Budget play the Rolling Stones' “You Can't Always Get What You Want” to callers on hold. But Mr Bush never gave Mr Daniels the latitude to make real cuts, because he was determined that everyone should get what he had promised them during his campaign.

Spending galore

The biggest handout was a prescription-drug entitlement for the elderly, known as Medicare Part D, which passed by a handful of votes in 2003. It addressed a real problem: some 22% of the elderly lacked drug coverage. But it did so in the costliest way imaginable. It is not means-tested, so old people who previously paid for their own drug coverage have an incentive to mooch off the taxpayer instead. It will cost an estimated $1.2 trillion over the first ten years—making it the biggest expansion of the welfare state since Mr Bush was dancing the Alligator at Yale.

The Bush Republicans passed the bill to woo the 40m elderly Americans, a group that seldom forgets to vote. Some were doubtless grateful, but since the plan started working this year, many have complained that it is confusing (which it is) and stingy (because it covers the first $2,250 of drug spending and anything over $5,100, but leaves a “doughnut hole” in the middle). Democrats, meanwhile, argue that the plan is too generous to drug companies. Voters seem to agree.

It came to a vote at 3 AM and after 45 minutes it was losing by four votes. Speaker Dennis Hastert and Majority Leader Tom Delay held the vote open for three hours while twisting a few arms, Rep. Nick Smith of Michigan claiming that campaign funds were offered in exchange for his vote, an account that he later recanted.

The cost estimate for the ten-year plan, initially pegged at $400 billion during Congressional debate, was revised to $534 billion after the bill was passed. Fiscally conservative Republicans may not have supported the bill with a higher estimate, one that government analyst Richard Foster apparently had at the ready but kept in his pocket for fear of losing his job.

The Economist reports the latest ten-year cost estimate as $1.2 trillion.

As for the performance U.S. economy under one-party rule, it all depends on who you ask. If you work on Wall Street, you'd probably say the economy has been good, but if you work on Main Street, you might have a differing opinion.

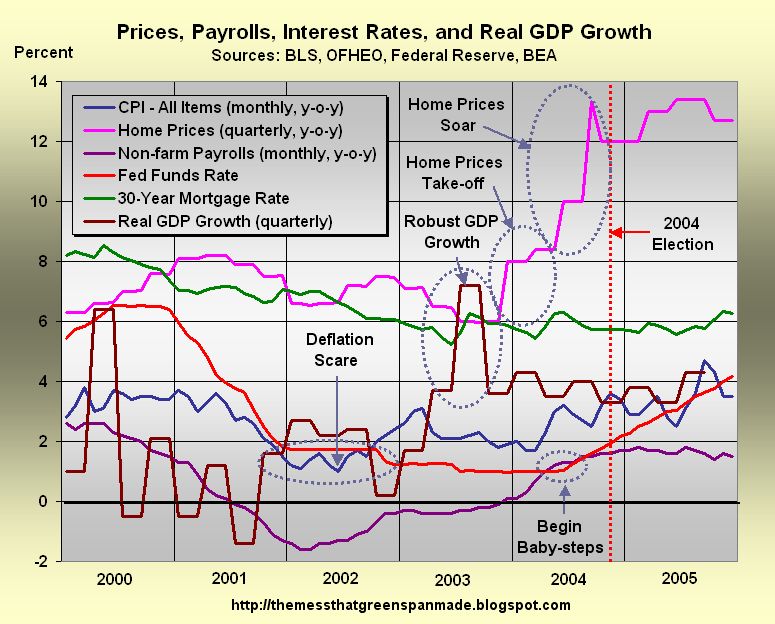

Despite economic statistics for which past presidents would give their eye teeth - an unemployment rate under five percent and both inflation and GDP growth near three percent - the booming economy has been a tough sell.By some measures, the economy has been doing quite well under the Republicans. Productivity growth has been strong, unemployment is low and inflation modest. Although output growth is slowing as the housing market slumps, petrol prices have plunged in the past couple of months and the stock market is up.

The difficulty in convincing the electorate that the economy is indeed going gangbusters speaks volumes about the current condition. Either the economic indicators are broken or there is a lag between the time that people realize there is something wrong and for this reality to show up in the data. Yet Americans are gloomy. Three-fifths of them tell pollsters that economic conditions in the country are getting worse, a much higher share than in 2004. Economists argue ferociously about how close this is to being true. The more dismal-minded ones point to average hourly wages, which rose by a slothful 0.6% annually between 2000 and 2006 once you adjust for inflation. Sunnier ones point out that if you include benefits, total hourly compensation rose by 1.3% a year over the same period. Yes, say the pessimists, but that is eaten up by soaring health-care costs. All right, say the optimists, let's look at consumption per head, which rose 17% in total between 2001 and the second quarter of 2006. Ah, say the doomsters, but that is because consumers are recklessly over-borrowing. No, say the optimists, it is because the Bush tax cuts left more money in their pockets.

Yet Americans are gloomy. Three-fifths of them tell pollsters that economic conditions in the country are getting worse, a much higher share than in 2004. Economists argue ferociously about how close this is to being true. The more dismal-minded ones point to average hourly wages, which rose by a slothful 0.6% annually between 2000 and 2006 once you adjust for inflation. Sunnier ones point out that if you include benefits, total hourly compensation rose by 1.3% a year over the same period. Yes, say the pessimists, but that is eaten up by soaring health-care costs. All right, say the optimists, let's look at consumption per head, which rose 17% in total between 2001 and the second quarter of 2006. Ah, say the doomsters, but that is because consumers are recklessly over-borrowing. No, say the optimists, it is because the Bush tax cuts left more money in their pockets.

Both sides make some valid points. But on balance the naysayers have the upper hand. The Bush economy has not felt great for most workers, for three reasons. First, at least until recently, workers' compensation has been surprisingly sluggish, while firms' profits are at a record high. Americans have kept up spending by borrowing, largely against the value of their houses. Their savings rate is now negative. Second, the gains of growth have been skewed to the highest earners. Rising income inequality means that average income can be growing smartly, even as most workers are not much better off. Third, as Jacob Hacker of Yale University points out, incomes are much more volatile than they were a generation ago. People may be better off, on average, but they worry more about losing their jobs, and with it their health insurance and their ability to pay their children's college fees. None of this helps the Republicans; polls show that Americans prefer the Democrats on every economic issue bar taxes.

The inflation indicator is clearly broken.

In recent years, many Americans have noticed how poorly the Consumer Price Index has tracked the price of things that they actually have to pay for. This was easy to overlook as long as home prices were included in the list of items that were going up in price, but with more and more homeowners realizing that their home really isn't an ATM machine that just keeps on giving, sentiment is shifting.

As for the employment picture, no one can really quarrel about job growth in recent years. The quality of the jobs is another matter - something that an increasing number of workers are also noticing, especially when meager pay increases of recent years are combined with rising prices.

Will divided government cure these economic ills? We are likely to find out soon enough.

I came to economics and the markets late in life. I started out as a midshipman at the Naval Academy, then migrated from learning to navigate the seas to navigating through the undergraduate basics of economics at Harvard. After a brief detour to Oxford—principally

I came to economics and the markets late in life. I started out as a midshipman at the Naval Academy, then migrated from learning to navigate the seas to navigating through the undergraduate basics of economics at Harvard. After a brief detour to Oxford—principally

The oddest part about the whole story is that, to this day, people still come to read it. A rough count of yesterday's traffic shows that about 60 people entered on this page. Sometimes, someone stumbles across it and posts a link on some other website apparently not knowing (or caring) that the story is almost a year old.

The oddest part about the whole story is that, to this day, people still come to read it. A rough count of yesterday's traffic shows that about 60 people entered on this page. Sometimes, someone stumbles across it and posts a link on some other website apparently not knowing (or caring) that the story is almost a year old.

Bednar recently talked to Newhouse News Service writer Sam Ali about the housing market, why he created his blog and the challenges of growing stony coral in his basement.

Bednar recently talked to Newhouse News Service writer Sam Ali about the housing market, why he created his blog and the challenges of growing stony coral in his basement.

If you just can't wait until the New Year to see what's over there (something to consider, given recent moves in uranium and precious metals), you can always request a free, no-obligation trial subscription by clicking

If you just can't wait until the New Year to see what's over there (something to consider, given recent moves in uranium and precious metals), you can always request a free, no-obligation trial subscription by clicking

China's massive hoard is the result of its large current-account surplus, significant inward foreign direct investment, and big inflows of speculative capital over the past couple of years. In theory, flows of foreign money into China should push up the yuan, but China has resisted this, forcing the central bank to buy up the surplus foreign currency. The growth in reserves has slowed in recent months, but it is still averaging a hefty $16 billion a month.

China's massive hoard is the result of its large current-account surplus, significant inward foreign direct investment, and big inflows of speculative capital over the past couple of years. In theory, flows of foreign money into China should push up the yuan, but China has resisted this, forcing the central bank to buy up the surplus foreign currency. The growth in reserves has slowed in recent months, but it is still averaging a hefty $16 billion a month. Nearly all of this data is available at the Federal Reserve website. The only part for which one has to look elsewhere is the last six months of M3 Money Supply - the central bank stopped divulging this data earlier this year.

Nearly all of this data is available at the Federal Reserve website. The only part for which one has to look elsewhere is the last six months of M3 Money Supply - the central bank stopped divulging this data earlier this year.