[This is the final installment in the series "Three Sins, One Gift" originally published one year and one day ago when Alan Greenspan retired as Federal Reserve Chairman.]

The Gift - Hastening the Demise of Fiat Money

Throughout history monetary systems have come and gone, though few people have understood what money is or how it works.

Through the ages, most people have been content to labor at their chosen craft in exchange for seashells, pieces of eight, or slips of printed paper, with the expectation that sometime in the future, these items could be traded for other goods such as food, clothing, or shelter.

Money is, and always has been, a medium of exchange - a way for people to trade their labor, or the fruits of their labor, for other goods that they want or need.

To most people, it's as simple as that.

A Store of Value

But, money is also a store of value. This characteristic is important because individuals may opt to save some of the money they earn in order to use it some time in the future. Workers have an expectation that money earned today will have a similar value in the future - that it will purchase similar goods in similar quantities.

How well a particular form of money serves as a store of value is related to the supply of money - how fast the supply of money increases.

Money maintains its purchasing power best when it is limited in supply.

This is basic economics - supply and demand. If, over time, money is created at an ever-increasing rate, there will be much more of it in circulation. Significantly more money competing for roughly the same amount of goods causes prices to rise and the money loses value.

But, forms of money that are limited in supply are often times impractical as a medium of exchange. One solution to this problem has been to use paper money "backed" by some item that is limited in supply. In this case, money consists of two parts - one that is easily exchanged and one that stores value.

For much of recent history, paper money has represented precious metal. The paper money could be exchanged with others to facilitate trade, and it could be redeemed on demand for the precious metal that backed it.

Paper money could be created only to the extent that precious metal existed and the amount of paper money in circulation was effectively limited.

Severing the Link

Since 1971 when Nixon closed the "gold window", there has been no link between paper money (or its electronic equivalent) and anything that is limited in supply.

The world now operates under a pure fiat money system where paper money is "backed" by nothing other than faith in the government that issues it. That is, faith in the government, the central bank, and regulatory agencies to limit the amount of money being created, lest it lose that very important quality as a store of value.

Throughout history, no system of fiat money has endured the test of time. There have been numerous examples, most notably in 18th century France leading up to the French Revolution.

The reason? It is too easy to create fiat money.

Governments create money to solve problems - wars, natural disasters, poverty, re-election. When money can be created "out of thin air" there is seemingly no limit to how much money can be created or how many problems can be solved.

Governments like to solve problems.

The world's money handlers profit by creating money to lend to businesses and individuals. When money, in the form of credit, can be created "out of thin air", there is seemingly no limit to the prosperity that can be fostered or the money that can be made.

Money handlers like to make money.

No one has benefited more from today's fiat money system than governments and the financial industry. Governments have borrowed and spent to please their constituents, and the world's money handlers have grown wealthy as few can imagine.

Not a Panacea

But, over time, fiat money proves it is not the great panacea that people at first think it is. In the broad sweep of history, its effects, though initially welcomed and embraced as hope for a new era of prosperity, prove fleeting.

Ultimately, despite what the government and the money handlers tell them, people come to realize that their money is losing its value at a quickening pace. It is losing value because too much of it has been created.

The words of the government issuing the money begin to ring hollow and the riches of the money handlers become far too egregious.

This realization comes to different people in different ways.

The poor usually suffer first and most, as they experience difficulty making ends meet. Their money no longer purchases what it once did. The poor have little understanding of history's broad sweeps, what money is, or what money once was. They know little of storing value.

Those in the middle may have prospered by participating in the speculative games offered up by the money handlers. Throughout history, rising asset prices fueled by the extraordinary creation of money and credit have provided the opportunity for ordinary individuals to obtain great wealth and notoriety.

Eventually, they too come to realize that their money has lost value and the lifestyle to which they have become accustomed can no longer be supported.

But, as in nearly all eras, the money handlers prosper more than all others. Those at the top - the business elite, the bankers, the peddlers of influence - they reap the benefits that fiat money provides, most of them knowing well its dark secrets and sordid past.

At some point in time, with a populace accustomed to ever-increasing prosperity and hope, fiat money fails to deliver.

The seams begin to bulge and the system becomes increasingly strained as ever-increasing amounts of fiat money must be poured into the economy to maintain its momentum.

The public becomes disillusioned, realizing they have been duped into behaving in ways that their forefathers would ridicule. Their profligate ways - lifestyles which don't square with incomes - give way to the harsh, cold reality that there is no free lunch and there are no easy riches.

They realize the government has mismanaged the nation's affairs, that the money handlers have once again benefited handsomely, and then there is unrest.

One thing leads to another, and one more fiat money system comes to an end.

The Greenspan Era

As the most powerful central banker in the world for nearly two decades, Alan Greenspan has done more than any other individual to increase the supply of money and credit in a world full of fiat money.

He has done more than anyone else to perpetuate the belief that creating money "out of thin air" can solve problems and that enriching the money handlers can benefit society.

He is, today, regarded by some as the greatest central banker of all time. But, the history books for this era have not yet been written - time has not yet passed judgment on his deeds.

Through the ages, man's tools and devices have changed, but his basic desires and weaknesses have remained. He is easily misled to believe things that he wants to believe, and the same hard lessons are re-learned over and over as the memories of previous generations fade.

In recent years, Alan Greenspan has provided much for people to believe in and many reasons to forget the past.

Because fiat money twists and distorts, changing how needs and wants are perceived and satisfied, the common man's reasoning ability is easily overwhelmed by the illusion of prosperity.

Alan Greenspan has done much to alter perceptions and maintain illusions.

The Gift

Ultimately, all fiat money systems are doomed. After all, politicians and money handlers are human, and when provided access to easy money to solve problems or garner profits, they will use it in ever increasing amounts until crisis ensues.

The fiat money system that Alan Greenspan inherited from Paul Volcker in 1987 was, however, a strange anomaly. It held promise. Its life expectancy had been extended through a stern paternal instinct and the meting of "tough love" during a tumultuous transition after breaking free from its gold tether sixteen years prior.

After punishing interest rates and much anguish, the system had been righted.

It appeared that the fiat money of the late 1980s would endure for generations - such a good job had Mr. Volcker done in quelling animal spirits and lowering expectations.

But those who had studied history knew that this would be a cruel joke to play on Mankind. The world's strongest economy, about to vanquish the evil Red Menace and stand alone in the world, operating with paper money backed only by promises?

Had Alan Greenspan meted pain as his predecessor did, administered "tough love" instead of appeasement, things may have turned out differently.

Had Alan Greenspan meted pain as his predecessor did, administered "tough love" instead of appeasement, things may have turned out differently.

But that was not his style.

Whether intentional or by happenstance, whether inspired by Ayn Rand and an Objectivist self interest, motivated by his early years as a gold bug, or driven by a simple desire to be popular, Alan Greenspan's actions have resulted in drawing nearer the end of another era of fiat money.

Alan Greenspan's gift to the world was to squash the hope that Paul Volcker's actions had augured - to bring nearer that eventuality that can not be avoided, and which should not be put off. For Man is Man - his tools have far outpaced his ability to reason and he is not suited for a world of pure fiat money.

No one knows what tomorrow will bring, but all signs indicate that the future of fiat money will not be one of enduring value. A generation of relative stability has begat instability.

Eventually, the current system of fiat money will give way to a new system, and this process has been by hastened by Alan Greenspan.

This was Alan Greenspan's gift.

Read more...

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

Mr. Logue quit his job as a real-estate agent near Fort Myers, Fla., in December. Then he set up shop as a franchisee of the dog-training chain Bark Busters. So far, he says, "I have zero regrets."

Mr. Logue quit his job as a real-estate agent near Fort Myers, Fla., in December. Then he set up shop as a franchisee of the dog-training chain Bark Busters. So far, he says, "I have zero regrets." Even before sales slowed, people in the industry said far too many agents were chasing too few deals. If hordes of inexperienced agents are scrapping for business, says Christopher Galler, a senior vice president of the Minnesota Association of Realtors, that can only lead to "a race to the bottom in fees."

Even before sales slowed, people in the industry said far too many agents were chasing too few deals. If hordes of inexperienced agents are scrapping for business, says Christopher Galler, a senior vice president of the Minnesota Association of Realtors, that can only lead to "a race to the bottom in fees." This week's bad news is said to be the U.S. "savings rate," which according to the official measure was "negative" for a whole calendar year for the first time "since the Great Depression," as Martin Crutsinger of the Associated Press helpfully put it. Hooverville, here we come!

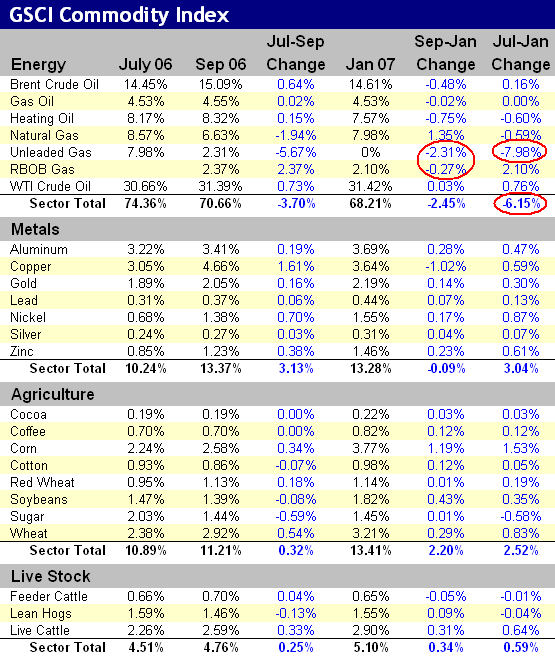

This week's bad news is said to be the U.S. "savings rate," which according to the official measure was "negative" for a whole calendar year for the first time "since the Great Depression," as Martin Crutsinger of the Associated Press helpfully put it. Hooverville, here we come! The GSCI, created in 1991, currently includes 24 commodities and is designed to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets.

The GSCI, created in 1991, currently includes 24 commodities and is designed to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets. The question remains how an index that is supposed to be

The question remains how an index that is supposed to be  FirstFed's foundation could crack even further. The biggest problem: Its mortgage portfolio is packed with risky loans known as option ARMS. These adjustable-rate mortgages allow borrowers to make smaller monthly payments than they would normally owe by deferring the principal and adding the difference back to the balance. That may make a house more affordable at first. But when the balance hits a certain level, payments often jump significantly, and borrowers can run into major financial trouble.

FirstFed's foundation could crack even further. The biggest problem: Its mortgage portfolio is packed with risky loans known as option ARMS. These adjustable-rate mortgages allow borrowers to make smaller monthly payments than they would normally owe by deferring the principal and adding the difference back to the balance. That may make a house more affordable at first. But when the balance hits a certain level, payments often jump significantly, and borrowers can run into major financial trouble. But skeptics are starting to question the quality of FirstFed's earnings. The bulk of FirstFed's income is derived from noncash earnings, largely from the deferred principal on its option ARMs. That so-called

But skeptics are starting to question the quality of FirstFed's earnings. The bulk of FirstFed's income is derived from noncash earnings, largely from the deferred principal on its option ARMs. That so-called  Still, given all the red flags, it's no wonder short-sellers have pounced. Some

Still, given all the red flags, it's no wonder short-sellers have pounced. Some  Some people we just write off as trust fund babies or hedge fund zillionaires or lucky dogs who got into the stock market at the right time and cashed out.

Some people we just write off as trust fund babies or hedge fund zillionaires or lucky dogs who got into the stock market at the right time and cashed out.

It is hard to argue with the statistics from the BLS as there are no real indicators to contradict their reports. Unlike inflation, where the "man on the street" would more likely differ with the government's account of rising prices, jobs appear to be plentiful in most parts of the country as confirmed by numerous consumer confidence surveys and anecdotal evidence. Whether the available jobs pay enough over the long-run to support rising prices is another matter.

It is hard to argue with the statistics from the BLS as there are no real indicators to contradict their reports. Unlike inflation, where the "man on the street" would more likely differ with the government's account of rising prices, jobs appear to be plentiful in most parts of the country as confirmed by numerous consumer confidence surveys and anecdotal evidence. Whether the available jobs pay enough over the long-run to support rising prices is another matter. Oil stocks did well as Exxon Mobil reported earnings for 2006 - about $108 million a day or $39.5 billion for the full year. Lots of companies would be happy with $108 million for an entire year.

Oil stocks did well as Exxon Mobil reported earnings for 2006 - about $108 million a day or $39.5 billion for the full year. Lots of companies would be happy with $108 million for an entire year. Gold tested $650 and retreated for the second time in the last two weeks - the third time's the charm. Don't worry about the IMF gold sales - they'll probably never happen, and if they do, China, Russia, the UAE, Argentina, and other central banks of resource-rich countries will be lining up to trade U.S. dollars for the shiny metal bars.

Gold tested $650 and retreated for the second time in the last two weeks - the third time's the charm. Don't worry about the IMF gold sales - they'll probably never happen, and if they do, China, Russia, the UAE, Argentina, and other central banks of resource-rich countries will be lining up to trade U.S. dollars for the shiny metal bars. The gold miners continue to be stuck in the mud - there will likely be a slingshot effect if gold and silver

The gold miners continue to be stuck in the mud - there will likely be a slingshot effect if gold and silver  And the dollar just hangs in there - looking quite good in comparison to the Yen lately. Those Japanese central bankers have got to be the worst in the world.

And the dollar just hangs in there - looking quite good in comparison to the Yen lately. Those Japanese central bankers have got to be the worst in the world. On a completely unrelated note, Punxsutawney Phil says, "

On a completely unrelated note, Punxsutawney Phil says, " And then there's the Russian central bank that has been talking about moving to a five or ten percent allocation of gold held as reserves. That would be a thousand tons more, not to mention the oil exporters in the Middle East who are having similar thoughts.

And then there's the Russian central bank that has been talking about moving to a five or ten percent allocation of gold held as reserves. That would be a thousand tons more, not to mention the oil exporters in the Middle East who are having similar thoughts. He followed in the footsteps of long-time Fed chairman Alan Greenspan, who stepped down after 18 years at the helm, leaving behind what many considered to be a troubled economy.

He followed in the footsteps of long-time Fed chairman Alan Greenspan, who stepped down after 18 years at the helm, leaving behind what many considered to be a troubled economy. Precedent seemed to suggest that equities were more likely to fare poorly after a series of interest rate hikes. The Dow Jones Industrial Average went on to make new all-time highs as 2006 drew to a close.

Precedent seemed to suggest that equities were more likely to fare poorly after a series of interest rate hikes. The Dow Jones Industrial Average went on to make new all-time highs as 2006 drew to a close. A rapidly rising gold price that appears ready to head even higher (maybe very soon) should give most any central banker reason to worry.

A rapidly rising gold price that appears ready to head even higher (maybe very soon) should give most any central banker reason to worry.