![[Most Recent Quotes from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sCJVwel4MMMpp3QR5zdqmV7ClPitBySZwddAK2EkYGvUmThTyCyTVaIElUYr30ocKymdkmXKzoNgxCYZuopPs6lgxwSyZXMJlBJuI34v4CkERe9NrdmUlLm8sXcqOd=s0-d)

![[Most Recent Quotes from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vLzi68eOnPPKDhBmv4LHd27_uNvc-xycUC9iWzi5hxjqeasGq_NmYj18t90IXpikU5jRK0EBy5DB5Vla7PbcXl88y-h0NgFixJ8hkD2wHWAJ5_gKDG6hh5k-cTDF3GLt0=s0-d)

![[Most Recent USD from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_s0DgmPxjsnT7n0c5Q_QgH1qhms_DjDCL6HdbeFapW7HSoYHRRSwNed82H5GYv5qL3PhARNbp7CZsJ5FL6X_nu-3y4WeddecykXUuTxIWOb9pgdHqvT0eiD=s0-d)

Equity Cushion Possibilities

Monday, October 10, 2005

The Rodriguezes seem like a nice family. They were featured in an article in yesterday's L.A. Times about homeowners who have run up sizeable balances on their home equity lines of credit, and now, faced with increasing short term interest rates, are refinancing this debt into new primary mortgages.

The sequence of events described in this story have no doubt played out many, many thousands of times around the country over the last year - homeowner taps equity and gets cash, homeowner gets easy interest-only monthly payment, homeowner repeats until monthly payments at new higher interest rates become bothersome, homeowner refinances.

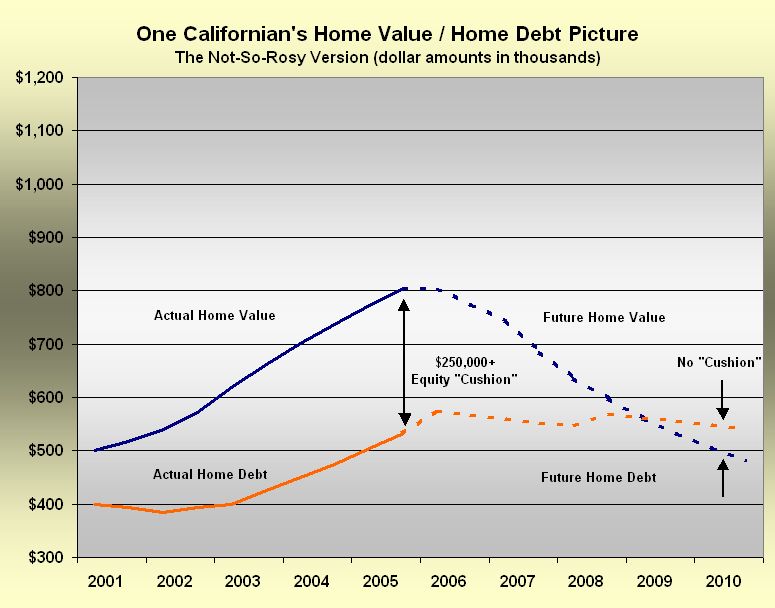

Yesterday's story tells of how the Rodriguezes bought a $500,000 home in 2001, then racked up $155,000 on a home equity line of credit, then refinanced into a new fixed-rate first mortgage on the same home now valued at $800,000.

What was the money used for?The 48-year-old mother of two had used the money for two new cars, kitchen renovations, investment in a family business and to help her oldest daughter through law school.

This is a success story in that the Rodriguezes are no longer exposed to rising short term rates and they still have a sizeable equity "cushion", as Fed Chairman Alan Greenspan calls it. But, what about the future?

With all the real estate "bubble" talk, it is natural to wonder what their future holds - to ponder what scenarios lie in wait, now that the ink is dry on their new loan - to wonder about the future of their equity "cushion".

Let's take a look at what the Rodriguezes have done and what they may think lies ahead for them - not from a monthly payment point of view (everyone knows that monthly payments go down after you refinance), but from an assets and liabilities point of view.

Using the data provided in this story we trace the last four years of home value and home debt, and project the future, as the Rodriguezes perhaps envision it.

Click to enlarge

Not bad! That's a nice equity "cushion" today, and the "cushion" in 2010 looks even better - the $155,000 withdrawal seems insignificant, almost as if it never happened. And, with a modest five or six percent per year appreciation (as recent surveys have indicated most homeowners expect), and with no new debt, things look even better five years out.

But what happens if the boom goes bust and in the years to come they are forced to tap their equity again - for some emergency or otherwise unforeseeable expenses?

What happens if prices decline like they did ten, fifteen years ago? In Southern California prices declined a total of 20 to 25 percent between 1990 and 1996 as can be seen here. In some areas, the decline was much greater - around 40 percent in some locales. And, this was after a run-up that was roughly a doubling of prices from the previous bottom - this time home prices have tripled since the real estate bottom in the mid 1990s.

The S&L bust that contributed to the previous decline may prove to have been fairly tame compared to what lies ahead - with all the wacky loans of recent years (interest-only, negative amortization, no-doc, etc.), and mounting questions of derivatives, the GSEs, and other possible surprises.

Chris Thornberg of UCLA Anderson Forecast notoriety thinks that homes may be overvalued by as much as 40 or 45 percent. What would that look like on a chart?

Let's see.

Let's look at an alternative scenario, one not nearly as rosy as the first one, regarding the Rodriguezes equity "cushion".

Click to enlarge

In this scenario, a 40 percent decline over a period of five years (surely, a future that very few Southern California homeowners are contemplating), the "cushion" appears to have gone flat. And, a couple more trips back to tap their equity in modest amounts has kept the debt at stubborn 2005 levels.

In this version of the Rodriguezes future, they may look back in a few years and regret having spent that $155,000 in the early part of the decade - perhaps coming to understand that they were duped into thinking that they had become blessed by enduring wealth.

In this scenario, like many others, the Rodriguezes may come to find that their wealth was ephemeral - that within the long sweep of real estate price trends, they were just caught up in a fleeting real estate enabled "wealth effect" like everybody else.

It is hard to resist the lure of so much home equity, just sitting there, begging to be used.

We will see - we wish the Rodriguezes well, they are not alone.

7 comments:

40% loss in nominal dollars over 5 years seems to extreme even for a bubblehead like myself.

The LA Times seems to be on a housing bubble kick. Todays "Business Section" (don't laugh, that little 6 page insert that is smaller than the Michaels ad is what passes for a business section in the LA Times) headlines an article entitled "Risky 'Exotic' Loans Fostering a Refi Cycle." The article says people are just swapping one IO ARM for anothere, postponing the day of reckoning, and leading to "interest only angst."

Then there's the front page, which has an article talking about how people are taking equity out through their lines of credit and investing it in . . . baja.

For me, the LA Times has always been a contrary indicator. When they talk about a market trend, you can usually count on it going the other way soon. I'm not sure what to make of it . . . could be that the party's about over.

David,

The forty percent number is from Chris Thornberg at UCLA - I didn't make it up - "overvalued by as much as 40 to 45 percent" is what he has said.

A year or so ago, I would have agreed with you about 40 percent being too extreme (maybe Chris Thornberg would have agreed too), but not today.

Since home prices have about tripled in the last ten years in this part of the country, consider that this house would have sold for maybe $260K in 1995-1996, then according to the article it was at $500K in 2001 and $800K now (I don't really believe the $500K and $800K numbers for 2001 and 2005 - prices have about doubled since 2001 no matter what area in Southern California you look at - see this link for the DataQuick historical prices. Plus, those numbers are too round - 500 and 800 - it's like the owner just guessed or the reporter tried to reconstruct it from memory).

For it to bottom at $480K in the next downturn would still leave it at almost double what it probably was at the previous low in the mid-1990s - I mean that's still a half million dollars!

For it to bottom at $480K in the next downturn would still leave it at almost double what it probably was at the previous low in the mid-1990s - I mean that's still a half million dollars!

But isn't that about what one would expect from 10 years worth of inflation? Isn't it the inflation effect that gives obvious truth to realtors' argument that RE never goes down (in the long run anyway).

Personally, the best thing we can hope for (IMO) is for prices to return to baseline and by "baseline" I mean what is implied by inflation.

"...coming to understand that they were duped into thinking that they had become blessed by enduring wealth."

You have your finger on the pulse of America with your "wealth effect" statement. The smart people bought assets with their equity cushion. The ones that purchased liabilities will have their day of reckoning.

Tim, I believe this is the real horror of the housing bubble. Regular families who are income and savings short have yanked money out of future appreciatian, in order to pay for todays expenses. I think that the problem is that with low interest rates, people felt they could amortize this debt without difficulty. This tremendous leverage is what is really going to be a disaster. Entering any kind of recession with excessive leverage is about the worst place you could be. If such a loss of equity did occur as you described, the economy would be in the toilet, and job will be lost. I believe this is the "debt liquidation" that your buddy AG was talking about. It may turn out to be quite ugly

If housing prices drop down to double, all that $$ that has vanished in value will make its way to other asset classes. Inflation will move and move quickly.

We've been lucky to have the release valve of the deficit to send all those new $$$ to Asia... but as this continues to vent, more and more of those dollars will come back chasing our goods and supply for things in truly in need.

That said, a residence may decline as noted. But a speculative vacation property or condo unit trading on condoflip.com will see the bottom drop out, while oil, gas, food and other essential recallibrate to the used and abused funny money dollar.

Post a Comment