![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

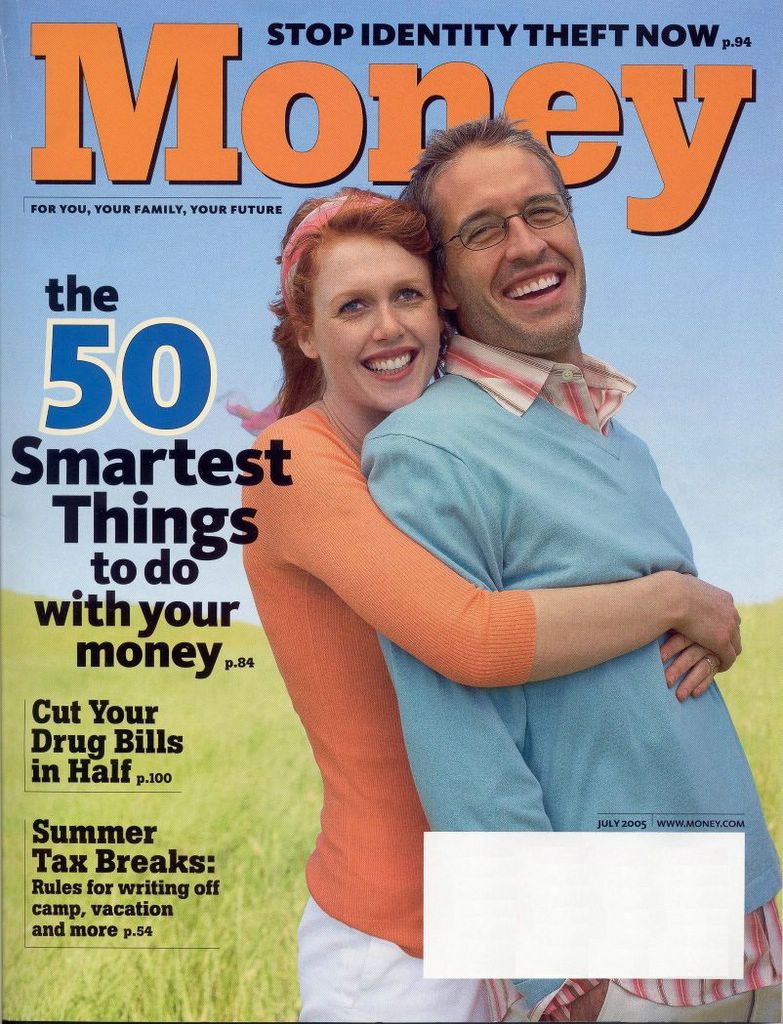

Why is This Couple So Happy?

Sunday, June 26, 2005

Click to enlarge

This couple is so happy because, on the advice of Money Magazine, they have opened up a home equity line of credit - they have done the number one "smartest thing" that they could do with their money.

Of the many "smart" things they could do with their money, the smartest things (according to Money Magazine) have to do with real estate - this is clear from the online version of this article. Right there at the top of the list is real estate - two steps above saving.

Of all the smart real estate related things to do with your money, in both the print and online versions, the "smartest thing" is:Do: Open a home-equity line of credit and use it for the right reasons: to tap as a rainy-day fund, to finance college for your kids or yourself, or to pay down credit-card debt.

This is Money Magazine mind control at it's best. This home equity - these tens or hundreds of thousands of dollars of asset inflation - this is YOUR MONEY. It's not just the increased value of an inflated asset that could continue to go up, or ... oh my! reverse course and go down - this is YOUR MONEY.

Don't: Raid your home's equity to fund vacations, plasma TVs and that Beemer you can't afford.

What's a little strange about this kind of money is that it has to be paid back. If you were to sell your house, you could get this money in cash - then it would be like other more traditional forms of money, like money in a savings account - money with no strings attached. But as home equity, this money has to be borrowed - but still this is YOUR MONEY.

[Actually, at a recent seminar, a Citibank mortgage representative referred to untapped home equity as "dead money" - money that is just sitting there "dead" - money that should be put to work - like for real estate investment property. This view seems to be institutionalized today - at least by lenders.]

While the obligatory warnings are offered - for the right reasons, rainy-day fund, college, pay down credit-card debt - we all know how this works. Shortly after this credit line is set up, it starts calling like a siren, beckoning to come and have some fun - come on, take a little and blow it on something, you know you want to.

Sometime after it is first tapped, there is a discernable change in one's standard of living. This can happen fast, or this can happen gradually - paying down credit card debt is so easy with a home equity line of credit. Running the balances back up only to have to pay them down again is easy too!

Even the warning, if parsed carefully, seems bent on influencing reader behaviour - don't "raid your home's equity", as if something short of a "raid" is OK. And don't spend this money on "vacations, plasma TVs, and that Beemer" - all things that people do anyway, knowing full well that it is wrong, maybe in defiance of authority, or maybe just because they are stupid.

Identified elsewhere in this article are many other genuinely smart things to do with your money - it is a shame that they have to start the discussion as they have, immediately recommending a home equity line of credit, something so easily abused, as the "smartest thing".

1 comments:

He's happy because he's scored a woman half his age. She's happy because she scored a sugar daddy.

Post a Comment