![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

The Issing Link

Monday, March 27, 2006

[From the March 25th edition of The Economist]

Money still makes the world go around. For some policymakers, anyway

TWO events in the past week highlight the huge divide in monetary policy thinking between Europe and America. On March 16th and 17th, a conference was held in Frankfurt to honour Otmar Issing, chief economist of the European Central Bank (ECB), who retires in May. Most participants agreed that central banks still need to watch the growth of the money supply. A week later, America's Federal Reserve stopped publishing M3, its broadest measure of money, claiming that it provided no useful information. Who is right?

Mr Issing was the architect of the ECB's monetary-policy strategy. He built it using a design taken from Germany's Bundesbank, where he was previously the chief economist. He holds two controversial beliefs that challenge prevailing monetary orthodoxy. First, he thinks that central banks must always keep a close eye on money-supply growth. Second, central banks sometimes need to lean against asset-price bubbles.

Consider the role of money first. Ask non-economists, “What is economics?” and they will often reply that it is “all about money”. Yet the odd thing is that the standard academic models used by most economists ignore money altogether. Inflation instead depends simply on the amount of spare capacity in the economy.

Nor does the money supply play any role in monetary policy in most countries, notably America. Alan Greenspan's last ten speeches as chairman of the Federal Reserve contained not a single use of the word “money”.

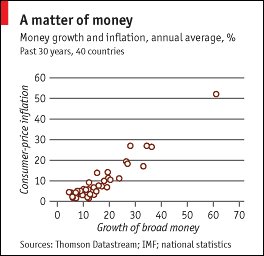

Yet Milton Friedman's dictum that “inflation is always and everywhere a monetary phenomenon” is still borne out by the facts. The chart plots the rate of inflation and broad money-supply growth in 40 economies over the past 30 years. In the long run, countries with faster monetary growth have experienced higher inflation. So why are central banks (except the ECB) paying so little attention to money?

The problem is that over short periods the link between the money supply and inflation is fickle, because the demand for money moves unpredictably. The Bank of England's early days provide a good example. Uncertainty over exactly when ships laden with valuable commodities would arrive in London could cause unexpected shifts in the demand for money and credit. The uncertainty was caused by many factors, notably changes in the direction and the speed of the wind as ships came up the river Thames. The bank's Court Room therefore had a weather vane (still there today) to provide a surprisingly accurate prediction of shifts in the demand for money. Sadly, no such gauge exists today. Financial liberalisation and innovation have also distorted measures of money, making monetary targeting—all the rage in the early 1980s—unworkable.

But it would be foolish to conclude that money does not matter. Throughout history, rapid money growth has almost always been followed by rising inflation or asset-price bubbles. This is why Mr Issing, virtually alone among central bankers, has continued to fly the monetarist flag.

The ECB's monetary-policy strategy has two pillars: an economic pillar, which uses a wide range of indicators to gauge short-term inflation risks, and a monetary pillar as a check on medium- to long-run risks. The monetary pillar has attracted much criticism from outside the ECB; it is often dismissed as redundant, if not confusing. It was originally intended to guard against medium-term inflation risks. More recently, Mr Issing has justified the pillar as a defence against asset bubbles, which are always accompanied by monetary excess.

Mr Issing's model is at last starting to win friends abroad. Julian Callow, an economist at Barclays Capital, sees strong parallels between the Bank of Japan's (BoJ) new monetary policy framework and that of the ECB. The BoJ has said that it will track the economy from two perspectives: price stability and growth one to two years into the future; and a broader assessment of medium- and longer-term risks, which is likely to include the growth of asset prices and credit. In his time at the podium at last week's conference, Kazumasa Iwata, deputy governor of the BoJ, seemed to confirm that the bank's new framework owed much to Mr Issing's legacy.

Pick your monetary metaphor

Unlike some central bankers, Mr Issing loves to be challenged, so he invited Don Kohn, a governor of the Fed, to tackle the ECB view that a central bank should sometimes “lean against the wind” to prevent an asset bubble inflating, by tightening policy by more than inflation alone would require. Mr Kohn argued the usual Fed line: because of huge uncertainties, it is too risky to respond to bubbles and therefore it is safer to “mop up” by easing policy after a bubble bursts. He tried to present the Fed's approach to asset prices as the neutral one, ie, less activist than the ECB's. But that is misleading. There is no such thing as “doing nothing”. Under the Fed's approach, unfettered liquidity sustains a bubble.

This link between money and asset prices is why the ECB'S twin-pillar framework may be one of the best ways for central banks to deal with asset prices. A growing body of academic evidence, most notably from economists at the Bank for International Settlements, suggests that monetary aggregates do contain useful information. Rapid growth in the money supply can often signal the build-up of unsustainable financial imbalances, as well as incipient inflation.

Charles Goodhart, a former member of the Bank of England's Monetary Policy Committee, mused in his speech to the conference that it would be deeply ironic if Mr Issing's departure coincided with a demonstration of the underlying worth of the monetary pillar. In other words, this may be precisely the wrong time to dismiss monetary aggregates: in these days of asset-price booms and imbalances, their informational content may be becoming more, not less, valuable. Will Mr Bernanke please take note?