![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

Equity Cushion Possibilities

Sunday, September 27, 2009

[You don't hear much about "equity cushions" anymore. Did anyone really understand what they were doing when this post originally appeared on October 10, 2005? It's a good bet that the Rodriguez family did not.]

The Rodriguezes seem like a nice family. They were featured in an article in yesterday's L.A. Times about homeowners who have run up sizeable balances on their home equity lines of credit, and now, faced with increasing short term interest rates, are refinancing this debt into new primary mortgages.

The sequence of events described in this story have no doubt played out many, many thousands of times around the country over the last year - homeowner taps equity and gets cash, homeowner gets easy interest-only monthly payment, homeowner repeats until monthly payments at new higher interest rates become bothersome, homeowner refinances.

Yesterday's story tells of how the Rodriguezes bought a $500,000 home in 2001, then racked up $155,000 on a home equity line of credit, then refinanced into a new fixed-rate first mortgage on the same home now valued at $800,000.

What was the money used for?

The 48-year-old mother of two had used the money for two new cars, kitchen renovations, investment in a family business and to help her oldest daughter through law school.This is a success story in that the Rodriguezes are no longer exposed to rising short term rates and they still have a sizeable equity "cushion", as Fed Chairman Alan Greenspan calls it. But, what about the future?

With all the real estate "bubble" talk, it is natural to wonder what their future holds - to ponder what scenarios lie in wait, now that the ink is dry on their new loan - to wonder about the future of their equity "cushion".

Let's take a look at what the Rodriguezes have done and what they may think lies ahead for them - not from a monthly payment point of view (everyone knows that monthly payments go down after you refinance), but from an assets and liabilities point of view.

Using the data provided in this story we trace the last four years of home value and home debt, and project the future, as the Rodriguezes perhaps envision it.

Click to enlarge

Not bad! That's a nice equity "cushion" today, and the "cushion" in 2010 looks even better - the $155,000 withdrawal seems insignificant, almost as if it never happened. And, with a modest five or six percent per year appreciation (as recent surveys have indicated most homeowners expect), and with no new debt, things look even better five years out.

But what happens if the boom goes bust and in the years to come they are forced to tap their equity again - for some emergency or otherwise unforeseeable expenses?

What happens if prices decline like they did ten, fifteen years ago? In Southern California prices declined a total of 20 to 25 percent between 1990 and 1996 as can be seen here. In some areas, the decline was much greater - around 40 percent in some locales. And, this was after a run-up that was roughly a doubling of prices from the previous bottom - this time home prices have tripled since the real estate bottom in the mid 1990s.

The S&L bust that contributed to the previous decline may prove to have been fairly tame compared to what lies ahead - with all the wacky loans of recent years (interest-only, negative amortization, no-doc, etc.), and mounting questions of derivatives, the GSEs, and other possible surprises.

Chris Thornberg of UCLA Anderson Forecast notoriety thinks that homes may be overvalued by as much as 40 or 45 percent. What would that look like on a chart?

Let's see.

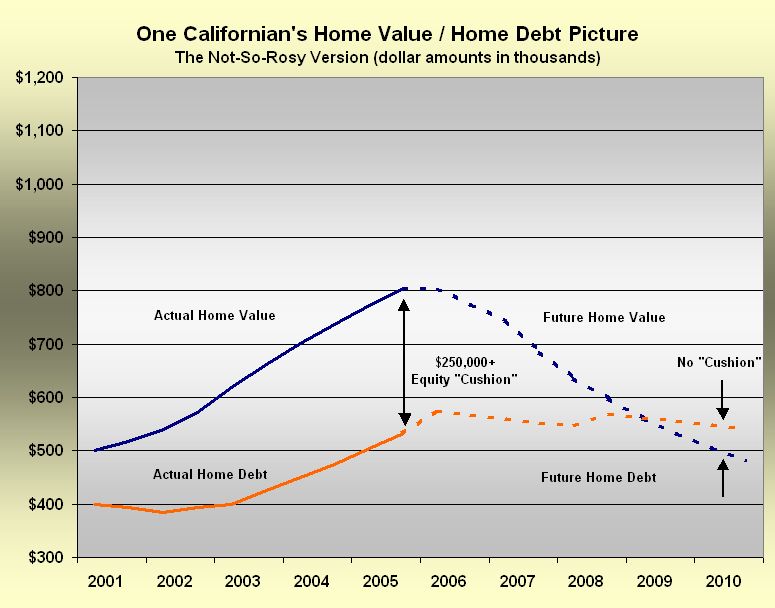

Let's look at an alternative scenario, one not nearly as rosy as the first one, regarding the Rodriguezes equity "cushion".

Click to enlarge

In this scenario, a 40 percent decline over a period of five years (surely, a future that very few Southern California homeowners are contemplating), the "cushion" appears to have gone flat. And, a couple more trips back to tap their equity in modest amounts has kept the debt at stubborn 2005 levels.

In this version of the Rodriguezes future, they may look back in a few years and regret having spent that $155,000 in the early part of the decade - perhaps coming to understand that they were duped into thinking that they had become blessed by enduring wealth.

In this scenario, like many others, the Rodriguezes may come to find that their wealth was ephemeral - that within the long sweep of real estate price trends, they were just caught up in a fleeting real estate enabled "wealth effect" like everybody else.

It is hard to resist the lure of so much home equity, just sitting there, begging to be used.

We will see - we wish the Rodriguezes well, they are not alone.

0 comments:

Post a Comment