![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

Inflation, Interest Rates, Game Theory

Friday, October 14, 2005

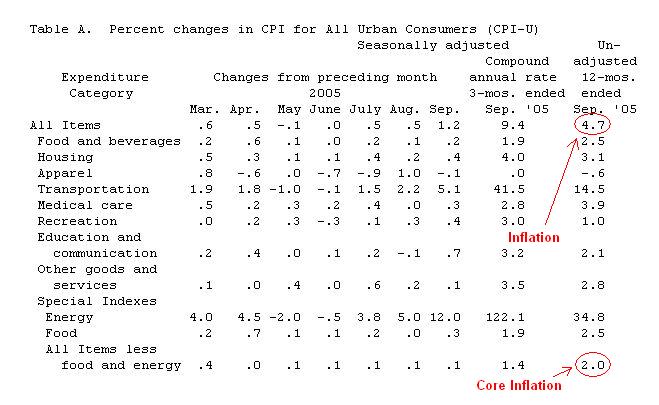

Today's inflation number came in at 1.2 percent for the month of September, making the year-over-year change to consumer prices a hefty 4.7 percent. The core rate of inflation, which excludes food and energy, came in at a benign 0.1 percent for September with a similarly benign annual rate of 2.0 percent.

There it is again - 2 percent inflation!

Click to enlarge

Not passing through ... benign ... long term inflation expectations remain contained ... non-inflationary growth ...

Just remember all that when you fill up your gas tank and pay to heat your home this winter.

Economists say that the core rate of inflation is more important than the actual rate of inflation because it provides a better indication as to where future inflation is headed, and serves as a better tool to formulate monetary policy.

While this may be true, the continued emphasis on core inflation has got to be a real slap in the face to middle and lower income individuals who find recent rises in their energy costs taking a proportionally bigger bite out of their income.

When our favorite CNBC star, Mark Haines, once again remarked on the stupidity of "core" inflation, Economist Drew Matus commented, "We're talking economics here, not common sense".

Enough said.

Interest Rates

Like central bankers, the conundrum that is long-term interest rates seems to respond to changes in the core rate of inflation as well. Yields dropped precipitously at the announcement of another in a long series of benign core inflation reports.

Generally, long bond prices have been falling a bit lately, causing yields and interest rates to move up. But, somehow it seems that long-term rates won't rise much.

Why would they?

Regardless of what inflation measure is used or what it indicates, who has an interest in long-term rates rising?

Who would sell off bonds in large quantities, knowing the impact that those actions might have on the world economy - rising mortgage rates in America, an abrupt end to the housing boom, the end of wealth-effect driven consumer spending, the end of the Asian manufacturing and export boom ...

Why would bondholders do something so foolish as to sell?

So what if inflation is 4.7 percent and U.S. Treasuries pay only 4.4 percent over ten years? Better to have no real return than to have no return at all, some might say. And, when a central bank is on the receiving end of said return, does the size of the return really matter? After all, central banks operate their country's printing presses and therefore have unique capabilities in compensating for poor returns on their investments.

Come to think of it, why do central banks need to worry about the return on their investment at all?

Game Theory

Currency and interest rate policies, as well as international trade relations, appear to have turned into the largest real-time game theory experiment the world has ever seen.Game theory is a branch of applied mathematics that studies strategic situations where players choose different actions in an attempt to maximize their returns. Although similar to decision theory, game theory studies decisions that are made in an environment where various players interact. In other words, game theory studies choice of optimal behavior when costs and benefits of each option are not fixed, but depend upon the choices of other individuals.

This thought is spurred by the recent Nobel Prize winners for economics - two elderly gentlemen who have done something in the field of game theory about which we know little, and seek to understand even less - the above excerpt encompasses all that we ever desire to understand about game theory:

Individuals acting based on what they expect others to do.

So, why would Japan or China sell bonds? Why would pension funds sell bonds? What would they do with the proceeds?

Buyers of Treasuries must understand that as long as interest rates are kept low, things will continue as they are - good for U.S. housing, good for U.S. consumption, good for Asian exports.

Similarly, they must believe that this can go on indefinitely - that Americans will continue doing what they have been doing ... forever.

This is where a problem may lie.

No one wants to do anything to spoil the party, so things keep getting a little more out-of-control until someone gets drunk enough to dive into the shallow end of the pool and cracks their skull. Then someone calls the paramedics so they can come and try to patch things back together before the drunk dies.

Or, maybe not.

Maybe someone comes to their senses and shuts down the party.

3 comments:

The people at The Economist are a bunch of Kohnheads.

http://www.economist.com/displaystory.cfm?story_id=5019763

so the swimming pool is like an ocean of debt and some drunk mistakenly dives into the short end - he thought he was buying long bonds but bought short-term bonds instead?

Good post. Your description of central banks unique capabilites helped me understand the conundrum.

If long rates stay low this winter, homeowners will be able to use their 'substantial equity cushion' to help heat their new (larger) homes.

Or they may even come to their senses and recognize their house is shelter and their perceived wealth (via equity) is the metaphorical wheelbarrow stacked full of paper…

Post a Comment