![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

Wither the equity cushion (revisited, again)

Thursday, February 07, 2008

In recent years (though not so much anymore), a central theme of Federal Reserve policy has been that homeowners have maintained a large enough "equity cushion" that whatever problems evolved in the nation's housing market would have a limited impact.

This view was originally offered up by San Francisco Fed Governor Susan Schmidt Bies and then codified by former Fed chairman Alan Greenspan in September of 2005:

In summary, it is encouraging to find that, despite the rapid growth of mortgage debt, only a small fraction of households across the country have loan-to-value ratios greater than 90 percent. Thus, the vast majority of homeowners have a sizable equity cushion with which to absorb a potential decline in house prices.The topic of "equity cushions" has been discussed on a number of occasions here and each time the basic premise was questioned, as in "What if home prices go down? What if home prices go down a lot?"

Of course, a couple years ago, the whole idea of falling home prices was laughable - home prices hadn't fallen nationally since The Great Depression.

How times have changed.

A quick search reveals the following pertinent posts, all of which help to explain the title of the post you are now reading.

- Sep 25, 2005 - Rationalizing Bubbles, Shaping a Legacy

- Oct 10, 2005 - Equity cushion possibilities

- Feb 09, 2006 - Leave your home equity alone!

- Nov 28, 2006 - Wither the equity cushion

- Aug 16, 2007 - Wither the equity cushion (revisited)

It didn't make sense then and it certainly makes no sense now.

And it seemed to be only a matter of time before mortgage lenders who have survived the housing market's fall thus far began reassessing those home equity lines of credit that were so generously extended some time ago when interest rates were low and home prices were still high.

Countrywide Financial was the big first lender to go public with announced changes last week, apparently in an attempt to "pretty up" the books before Bank of America completes its acquisition:

- Feb 1, 2008 - Trying to tap into home equity? We'll see

- Feb 1, 2008 - Lenders freeze equity lines in response to tumbling property values

- Feb 2, 2008 - Home equity borrowers get iced out

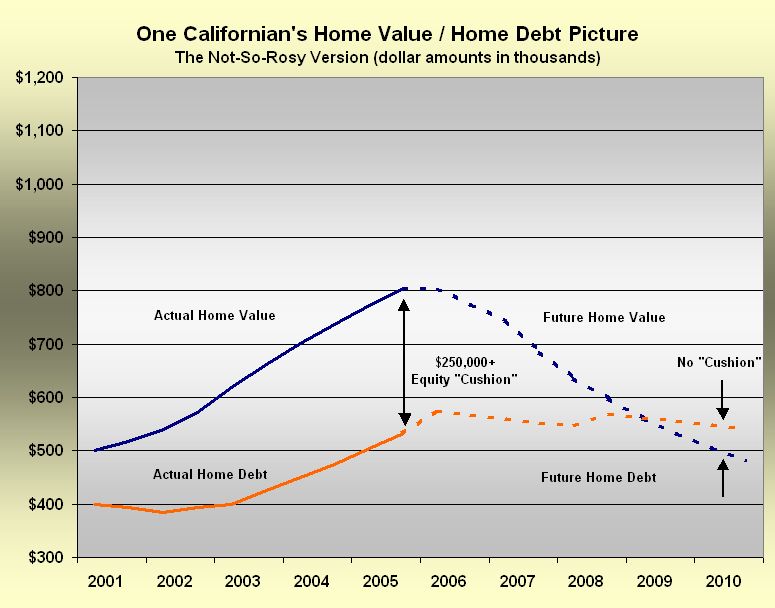

Has anyone heard anything on the Rodriguez family in Los Angeles, the subject of the late-2005 post, "Equity cushion possibilities"?

Two scenarios were contemplated at the time, the rosy scenario:

Click to enlarge

And the not-so-rosy one:

Click to enlarge

Boy, those old charts are just awful looking.

1 comments:

This chart is my take on the lending picture, from the most recent Federal Flow of Funds report. (I doubled 3Q07 to estimate FY07 because 4Q07 numbers are coming in March).

IMO, how low the downslope goes will determine the amount of bubble lending and underwater buyers (basically draw a horizontal connecting line leftwards from the most recent data point until this line intersects the upward slope; the curve area above that connecting line is a rough estimate of the amount of unsupportable bubble lending).

Post a Comment