![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

If not the Fed, then who?

Tuesday, August 18, 2009

[This missive was originally published more than four years ago on August 2nd, 2005.]

As the consensus grows that the complete inflation of another asset bubble draws near - first stocks, now housing - many financial writers and elected officials are asking the question, "Why hasn't the Federal Reserve done something about all the crazy lending practices fueling the housing bubble?"

During the Humphrey-Hawkins testimony a couple weeks ago, Congressman Jim Saxton asked a number of questions (pdf) of Federal Reserve Chairman Alan Greenspan regarding banking regulation as it relates to current lending practices. As detailed in yesterday's fine post by Calculated Risk over at Angry Bear, it seems that the short answer from the Fed is, "That's not my job".

The Federal Reserve is apparently not much interested in the goings on at local real estate offices and mortgage lenders and is, to a large degree, turning a blind eye to the absolutely wacky home prices and lending terms that have developed in recent years. Their interest is in the soundness of the banking system - the monitoring of reserve requirements and mortgage delinquencies and default rates, which to date have not been problematic.

A few months ago the Federal Reserve and a number of other agencies issued guidance regarding home equity lending, but as reported in the New York Times recently, these guidelines seem to have been largely ignored.

So where does that leave us? Everyone cross their fingers and hope for the best?

Or, as Mr. Greenspan commented a few months back, "If there's a crisis, we'll all get together and solve it - or hopefully solve it."

A Few Examples

In what is probably the best example of the lack of effectiveness of the Home Equity Lending Guidelines from a few months back, a recent radio advertisement for a local Southern California lender hawking home equity loans made very clear that the only thing required to get a new home equity loan was equity in your home. You don't need a job or good credit - apparently all you need is an appraisal and your most recent mortgage statement. They'll take it from there.

But, it is not the Fed's job to do anything about this - they've issued guidance.

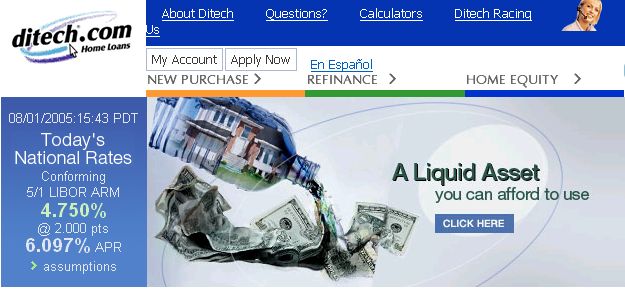

One of the better graphics to illustrate the home equity borrowing phenomenon is at Ditech.com, where they fancy rising home prices as something that can be stored in a bottle, then dispensed as necessary whenever the homeowner desires:

Click to enlarge

That's a house inside the bottle, and it is pouring out money. Nice!

Along with GMAC, Ditech.com is about the only part of General Motors that is profitable these days, and it is more than ironic to hear ads for Ditech.com home equity lines of credit intermingled with debt counseling ads on radio and television - kind of a like a choice between more booze or some freshly brewed coffee. Most people probably choose the former.

Again, not the Fed's job to discourage this sort of thing - the banks are sound.

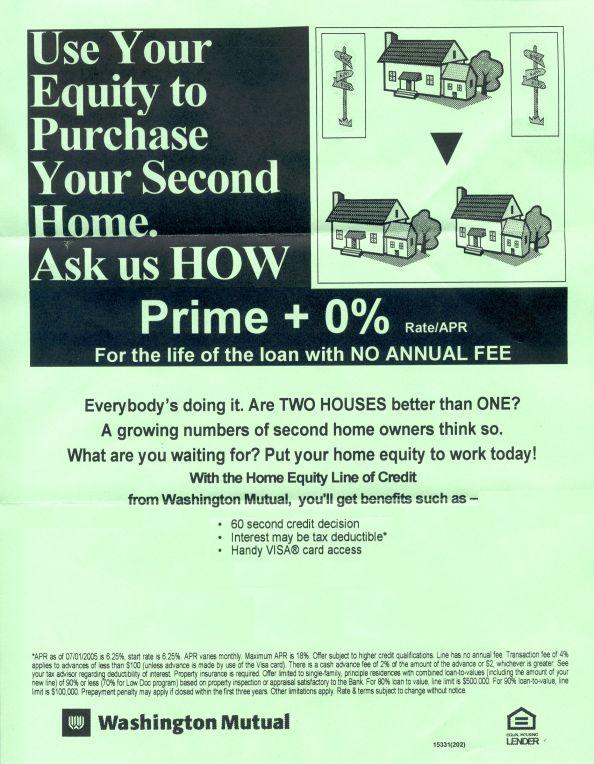

And finally, showing up in the mailbox yesterday was this gem from Washington Mutual:

Click to enlarge

Another nice graphic - this one more for its simplicity rather than the actual artwork - one house turns into two houses. And, it's OK because "Everybody's doing it. What are you waiting for?"

If not the Fed, then whose job is it to protect today's lenders and borrowers from each other?

You'd think that if no one wants to regulate lending practices, the least they could do is regulate lending advertising. That would be a good start.![]()

1 comments:

http://www.auditthefed.com/

http://www.youtube.com/watch?v=e3zo7zjYk2E

Post a Comment