![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

This May Take a While

Wednesday, April 19, 2006

Dataquick reported March real estate sales data yesterday, the headline somewhat casually announcing that the median price paid for a Southern California home has reached the half million dollar mark for the first time ever.

Notably, this report shows monthly mortgage payments rising briskly along with interest rates and prices - the typical monthly mortgage payment (well, not really typical - few people use conventional loans anymore) went from $2251 in February to $2383 in March.

It's not clear how this was calculated and the February sales data for Southern California, reported in March, is mysteriously missing from the DataQuick website, but it's a safe bet that this is the standard 20 percent down, 30-year fixed calculation. If so, that puts the interest rate at just under 6 percent, meaning that this month's slightly higher mortgage rates will result in another hundred dollars or so added to this typical payment in next month's report.

Homebuyers who actually used this financing would have a PITI (principle, interest, taxes, and insurance) of just over $3,000 or $36,000 per year, meaning that, in order to qualify for this loan under the 1990s guidelines of no more than 28 percent of gross income for this purpose, gross income would need to be almost $130,000, which is more than double the median household income for this area.

How times have changed.

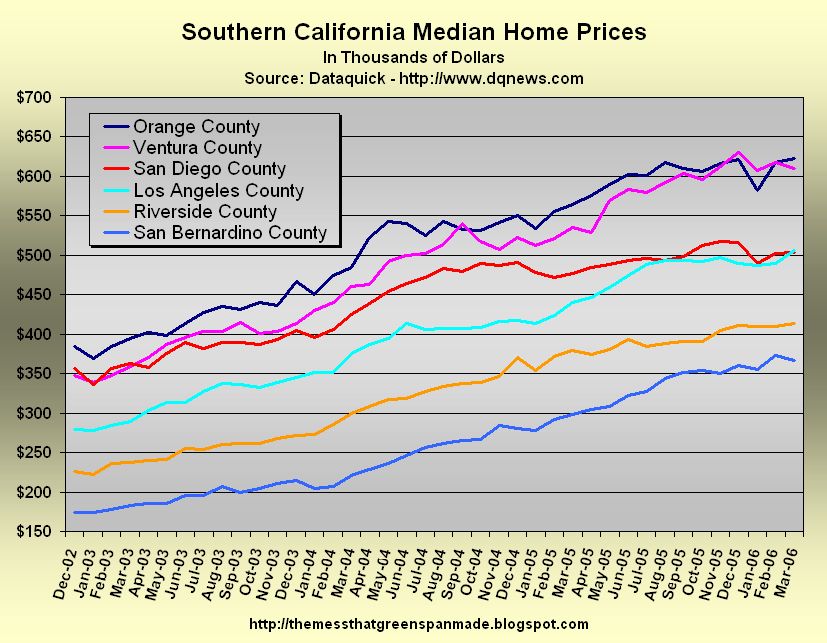

The median prices by county are shown below - Orange and Ventura County continue to tango, while Los Angeles and San Diego battle for third most expensive county. Click to enlarge

Click to enlarge

In a picture almost too good to be true, San Diego is (so far) pulling off the much hoped for soft landing while the other counties head inexorably toward single digit appreciation, Riverside County picking up more downward pace recently. It seems this whole process, wherever it leads, is going to take a while. Click to enlarge

Click to enlarge

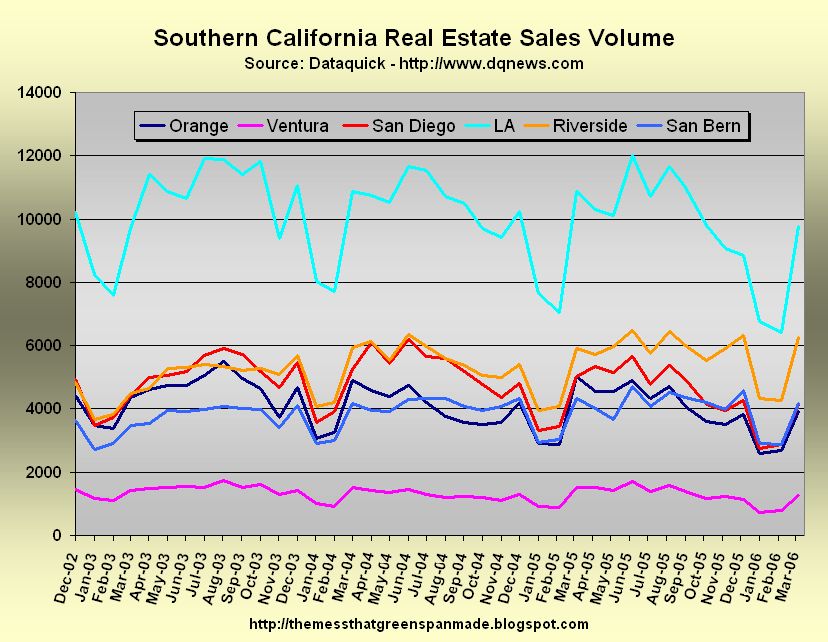

Volume rebounded smartly, though not to previous levels, Riverside County being the exception. It's funny how Riverside County has the best volume trend but the worst price trend. Well, maybe it's not funny, but it sure is interesting. If anyone from the Riverside area has an explanation for this, please share. Click to enlarge

Click to enlarge

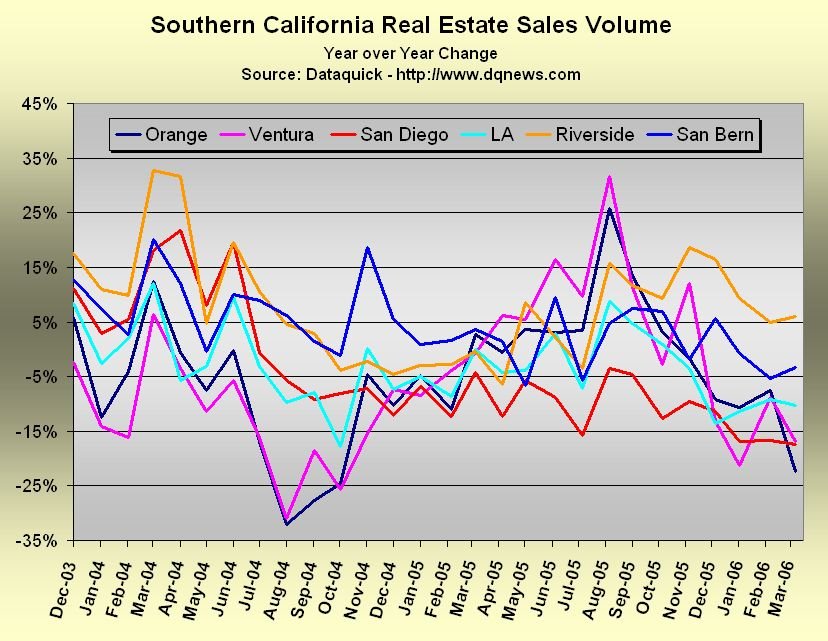

Here, the Riverside County year-over-year volume change is the only one that has remained positive in recent months. Rising volume, slowing appreciation - very curious. Click to enlarge

Click to enlarge

The longer this goes on, the more it seems that Southern California is different from the rest of the country in that the buyers keep coming and high prices stay high, regardless of interest rates. As long as there is credit available, there appears to be no shortage of borrowers who take whatever terms that will secure the home loan they desire.

Last October, the BusinessWeek real estate blog posted the following letter from a local attorney:I am a lawyer and I represent illegal aliens in deportation. In all but one of 35 cases I currently have on docket the illegal owns a home. But it is the loan terms that fascinate me. One lady finished school at second grade, speaks no English, and works for a recycling company binding cardboard boxes. She makes about $30K per year and is a single mom with three children. She has a $430K interest only loan that she used last year to buy a $430K condo - 100% financing - she paid $3,000 in closing costs. I tried to explain that her monthly payments will rise substantially in four years. She does not believe me, did not understand what I said and told me the loan and real estate agents specialize in real estate and would have told her if her payments could go up. If 34 of my clients with risky loans and no school past at best eighth grade are surprised by rising loan payments, we should be afraid. This is the last group desperate lenders pander to, meaning we're near the end.

You have to wonder how much this sort of thing accounts for the resiliency of the Southern California real estate market, but more importantly, what it portends for future home prices.

4 comments:

Since San Diego pulled up from its imminent zero crossing last September/October, you've gone soft on the whole impending doom angle. Can't say that I blame you. Can't say that I really trust DataQuick either.

At least we don't have to worry about the median income household not being able to afford the median house. They don't have to because they already own one.

36k per year PITI is easily do-able for a 90k per year family, representing 40%, if they aren't carrying auto or cc debt.

I almost hate to say this, and I definitely mean you no disrespect, but you just don't "get it" with respect to the housing "bubble", and you never have.

Major props to you for not burying your error, though, and for keeping up with the charts as they are an extremely useful resource.

Cheers!

I see charts and discussion for PRICES and SALES VOLUME and their delta.

Where are the charts for per-county inventory levels and foreclosures?

Post a Comment