![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

The Keystone Inflation Cops

Tuesday, June 27, 2006

The ongoing debate about the many ways to measure "inflation", the definition of the word "inflation", and the ruckus regarding owners' equivalent rent as it relates to said measures of "inflation" are all starting to make the nation's economists look like Keystone Cops. Having never met an economist, and having no particular axe to grind with them as a group, the objections voiced here spring almost entirely from looking at their work through the eyes of an engineer. That is, through a lens of scientific rigor that seems to be completely absent from the dismal science, at least when it comes to that one special word - inflation.

Having never met an economist, and having no particular axe to grind with them as a group, the objections voiced here spring almost entirely from looking at their work through the eyes of an engineer. That is, through a lens of scientific rigor that seems to be completely absent from the dismal science, at least when it comes to that one special word - inflation.

After hearing Steve Liesman on CNBC once say, "I'm an economist, I'm not supposed to make sense", when responding to a particularly sharp objection to his musing on this subject, a parallel can be drawn to say, an engineer at NASA replying in the same manner when queried on a controversial technical aspect of a Space Shuttle flight. You just wouldn't hear that sort of answer.

Granted, economics isn't a hard science, but it's not astrology either.

In recent weeks, on the subject of "inflation", more and more words have been expended in an attempt to explain what may be going through the minds of the economists at the Federal Reserve, raising doubts in the minds of many as to whether anyone has their hand on the rudder of the ship otherwise known as the U.S. economy - or if there is a rudder at all.

The Economist magazine weighs in on the debate over core inflation and owners' equivalent rent in the current issue's Feeling the heat where they note that the boys at the Fed have been "seized by a sudden panic" - not the kind of description normally applied to the staid types at the august Board of Governors.CENTRAL bankers are supposed to be calm, even a little boring. But the governors of America's Federal Reserve seem to have been seized by a sudden panic about inflation. Virtually every Fed official has been worrying aloud about rising prices. Ben Bernanke, the Fed's chairman, warned about “unwelcome” inflation on June 5th. Since then his colleagues have declared it to be “troubling”, beyond their “comfort level” and even “corrosive”.

We'll get to all the other measures of inflation in a minute, but first note that chart above looks a bit familiar and for good reason - a larger version of similar data appears below and was part of a story here last week, How Not To Fight Inflation.

...

The central bankers have clearly been spooked by the recent jump in the “core” consumer price index (CPI). The core measure excludes the volatile prices of energy and food. Over the past three months this index has risen at an annual rate of 3.8%, the fastest in more than a decade.

But much of that jump is thanks to a sharp rise in the cost of housing (which makes up almost 40% of core CPI), particularly the category of “owners' equivalent rent” which estimates the cost of living in a house by looking at rents charged on similar properties. Although this measure makes sense in theory (by living in your house you forgo rental income), it may now be overstating inflationary pressure.

As the housing market has slowed, fewer people are buying property, choosing to rent instead. That has pushed up rents. In turn, owners' equivalent rent has risen too, even though homeowners have seen no change in the actual costs of owning their house. Because owners' equivalent rent is estimated net of utility prices, recent falls in gas and electricity bills have paradoxically made matters worse. Statistical quirks, in short, are distorting the picture. But what should central bankers do about it? Some suggest that owners' equivalent rent should simply be dropped from the inflation index. That is what European statisticians have done. But credible central bankers cannot suddenly ignore an inflation component when it starts behaving in ways they do not like. That was the mistake made in the 1970s, when officials deluded themselves that inflation was under control by excluding ever more prices from their indices.

Statistical quirks, in short, are distorting the picture. But what should central bankers do about it? Some suggest that owners' equivalent rent should simply be dropped from the inflation index. That is what European statisticians have done. But credible central bankers cannot suddenly ignore an inflation component when it starts behaving in ways they do not like. That was the mistake made in the 1970s, when officials deluded themselves that inflation was under control by excluding ever more prices from their indices.

The bigger point is that even if you take out housing costs the recent acceleration in core consumer prices does not disappear (see chart). And a variety of other gauges suggest that underlying inflation is on the high side and rising. The deflator for core personal-consumption expenditure (PCE), Fed officials' favoured index, was up 2.1% in the year to April. The “trimmed-mean PCE deflator”, calculated by the Dallas Fed, which excludes those prices that have risen and fallen the most before taking a weighted average of the rest, is up 2.4%. The “median consumer-price index”, calculated by the Cleveland Fed, is up 3%. Look at these figures and the surprise is less that the central bankers are now so jumpy about inflation than that they sounded so sanguine earlier this year.

For some reason, in the chart from The Economist, they've chosen to exclude both rent and owner's equivalent rent, whereas in the chart below, only owners' equivalent rent is omitted. This yields a much different conclusion - the annual rate of increase of core CPI without OER has declined from almost 2.5 percent to near 2 percent in the last year and a half when omitting only owners' equivalent rent.

Let me repeat.

If you exclude owners' equivalent rent - what many feel is a completely useless indicator in light of what has transpired in the U.S. housing market in recent years - the annual rate of increase of core CPI has been declining for a year and a half.

Why the economists at The Economist chose to muck up the discussion by excluding real rent paid by real renters (in addition to excluding owners' equivalent rent) is a mystery, but they have only made the inflation chase that much more Keystone-like. Click to enlarge

Click to enlarge

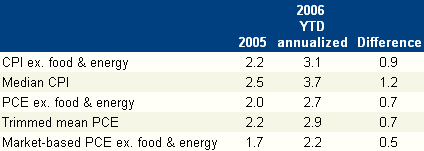

As for alternate measures of inflation, the Dallas Fed has provided a neat summary of the situation in Parsing Recent Inflation Data. This inspires little confidence that anyone is getting any closer to any answer about what "inflation" is, how it should be measured, or how it might be dealt with if indeed it is a problem.Measured core consumer price inflation has picked up noticeably over the past few months. The following table compares inflation over the 12 months of 2005 with annualized year-to-date inflation in several core consumer price indexes.

What is sorely needed here is a "grand unification theory" for inflation - sort of like the quest to unify the forces of nature (e.g., electromagnetism and the nuclear forces) into a single coherent theory - something more elegant and more beautiful. What’s going on here? Some analysts have suggested that the primary culprit behind the recent surge in core rates is a sharp increase in the price index for owner-occupied housing. For the PCE, at least, this is not the case. While the price index for owner-occupied housing has contributed somewhat to the recent surge, the pattern of increase in the core PCE remains even if owner-occupied housing is excluded from the index.

What’s going on here? Some analysts have suggested that the primary culprit behind the recent surge in core rates is a sharp increase in the price index for owner-occupied housing. For the PCE, at least, this is not the case. While the price index for owner-occupied housing has contributed somewhat to the recent surge, the pattern of increase in the core PCE remains even if owner-occupied housing is excluded from the index.

Perhaps someone could come up with a new measure of inflation that would unify the competing theories - it might be called the market-based median trimmed mean CPI (ex. food & energy).

And, maybe not.

Last, but certainly not least, and consistent with views held by current Fed Chief Ben Bernanke that however "inflation" is measured it is still overstated, come these words of wisdom from Robert Gordon of Northwestern University - Has Anybody Told the Fed?A 1996 report by a commission headed by Michael Boskin, a Stanford economist and chairman of the Council of Economic Advisers for President George H.W. Bush, said the CPI overstated inflation by 1.1 percentage points. The Bureau of Labor Statistics subsequently tweaked the CPI, accepting some of the commission’s suggestions and making other changes that it had been contemplating itself.

What do consumers know anyway?

In a new National Bureau of Economic Research working paper, Gordon revisits the commission report and subsequent changes to the CPI and related research. “My own retrospective view is that the upward bias in the CPI in 1995-96 was if anything higher than the Boskin (commission) estimate of 1.1 percent and was perhaps 1.2 or 1.3 percent,” he says. Given the changes made since, and applying an approach similar to Boskin commission, he estimates the CPI currently overstates inflation by about 0.8 percentage points, a view that runs counter to frequent consumer complaints that the CPI understates the inflation rate they face.

They don't have all the data that economists have and they don't have the analytical tools to properly calculate something as complex as "inflation". All consumers know is what they pay for things - like gasoline, heating oil, medical insurance, housing, and the many other items that continue to rise in price.

The calculation of "inflation" is best left to the professionals who can properly adjust the prices actually paid by consumers and put them into a broader context, though they are having a difficult time lately explaining themselves.

So, is inflation rising or falling? Is it overstated or rightly stated and by which measure?

Dunno.

Just don't ask a policeman if he's wearing a funny hat.

12 comments:

"If you exclude owners' equivalent rent ... core CPI has been falling for a year and a half."

Wrong. You mean to say that the rate of increases in core CPI have been falling. Core CPI still increased throughout that period.

Maybe Bernanke is just preparing us for what he's about to do: print craploads of money.

This will certainly cause inflation.

I don't know CPA - the CPI is a rate of increase (e.g., two percent per year). Substitute rate of increase for core CPI and it makes sense to me:

"If you exclude owners' equivalent rent ... the rate of increase has been falling for a year and a half."

Maybe "declining" would have been a better word than "falling" - I'll make that update so as not to confuse falling prices with a declining rate of increase.

Isn't the grand unified theory of inflation that you mention actually just the rate of change in M3? Problem solved... Now, we just need to the fed to start publishing all of the M3 components again.

Do you really have to be an economist to recognize inflation?

I can just look at the world around me and know that its pricey and the consumer is dead.

To my eyes (I left LA for four years for work) the economy in LA is already on its ear. I've never seen such a grotesque increase in prices over such a short period of time in all my life. I've got friends who weren't able to earn as much as me (their incomes stayed flat) who are selling off assets like Michael Jackson just to stay afloat.

Again, do you really have to be an economist to recognize this?

Is the US economy in a recesssion or not?

If you don't know the rate of inflation, how can you tell if the GDP is growing or contracting.

Grand theory of inflation? I think the Austrian economics guys already figured all that out ... in wholesome rigor. It's just that people don't like the answer.

So, the rest of these jokers are still trying to convince everyone that the world is flat, energy is not conserved, and build the economic perpetual motion machine.

Steve Liesman's not an economist -- he's a journalist pretending to be an economist. From his bio:

Liesman holds a Masters of Science from Columbia University Graduate School of Journalism and a B.A. in English from the State University of New York, Buffalo.

Degrees in journalism and English do not an economist make. Not that he's a bad economic journalist -- just that I don't think he could make it through the writings on inflation of _real_ economists like Michael Woodford or Thomas Sargent.

That's probably only because Woodford and Sargent, not being journalists or english majors, probably can't write a coherent sentence, not because Liesman wouldn't be able to understand them if they could.

"the CPI is a rate of increase (e.g., two percent per year)"

No it's not. The CPI is an acronym for Consumer Price Index. From Wikipedia: CPI is a "...weighted average of prices of a specified set of goods and services purchased by wage earners in urban areas. It is a price index which tracks the prices of a specified set of consumer goods and services, providing a measure of inflation"

What is often reported in the media is the change in the CPI, not the CPI itself.

Here's the government's FAQ. Question #13 I thought was helpful to our discussion.

I stand corrected - thanks for clarifying this.

I've updated the text to say "annual rate of increase of core CPI" - I guess I always think of inflation and the price indices as if they were the same, where saying CPI just specifies which price index is being used to measure of inflation.

We've all been trained to think of inflation and the price indexes as being the same. This is so they can modify the metric to distract us from what's really happening.

It's not because people don't want to understand inflation. It's because they have been conditioned with misinformation and tactical confusion. It's on purpose.

Inflation is the rate of change in M3. Period.

If you "park" some USD under the mattress, then it won't show up in the CPI. Or you could "park" that USD in asset prices. Or you could "park" it in oil prices. Or "park" it in central bank reserves...

But with their confusion tactics, the Fed can say: "look at the CPI, no inflation!"

When will people wake up to this?

The Fed lies. Pure and simple.

Post a Comment